From ashes to recovery: Inside the dramatic transformation of crypto lending through enhanced security, regulatory compliance, and new business models designed to restore investor confidence

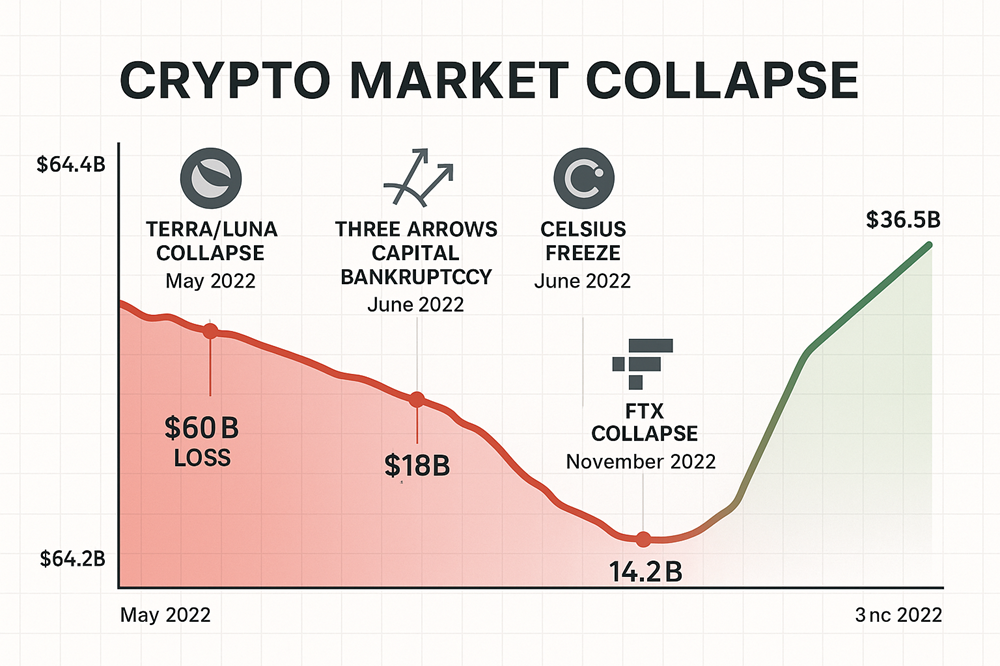

The numbers tell a brutal story. The crypto lending market peaked at $64.4 billion in Q4 2021, then collapsed to $14.2 billion by Q3 2023 — a 78% wipeout that left millions of investors burned and an entire industry questioning its foundations [1]. But here's what the data also shows: by Q4 2024, the market had clawed back to $36.5 billion, representing a 157% recovery from its lowest point [1].

This isn't just another comeback story. The platforms driving this recovery have rebuilt their operations from the ground up, implementing safety measures that would have been unthinkable during the reckless growth years of 2020-2021. The question facing investors today isn't whether crypto lending can work — it's whether these new models can maintain their discipline when the next bull market tests their resolve.

The Domino Effect That Changed Everything

The collapse didn't happen overnight. It started with Terra's algorithmic stablecoin UST losing its dollar peg in May 2022, wiping out $60 billion in market value and exposing the fragility of interconnected crypto financial systems [2]. Three Arrows Capital, a hedge fund with $18 billion in assets, became the next domino to fall, defaulting on loans from virtually every major crypto lender [3].

But the killing blow came from FTX. When Sam Bankman-Fried's exchange filed for bankruptcy in November 2022, it revealed an $8 billion hole in customer funds and triggered a liquidity crisis that brought down platforms across the ecosystem [4].

BlockFi, which had received a $400 million credit line from FTX, filed for bankruptcy within weeks [5]. Celsius had already frozen withdrawals in June, eventually revealing $2.8 billion in liabilities against $2.6 billion in assets [6].

"The 2022 collapse exposed systemic vulnerabilities in centralized lending models, eroding trust in platforms like Celsius and BlockFi," according to AInvest's analysis of the crisis [7]. These weren't just business failures — they were architectural collapses of the entire risk management framework that underpinned crypto lending.

Risk Management Revolution

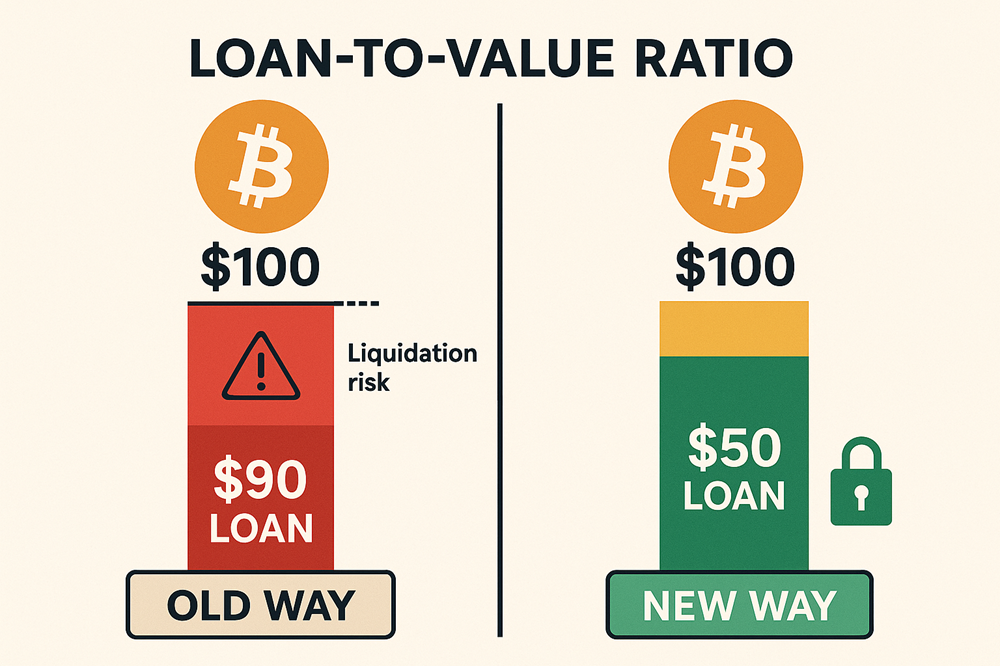

Today's surviving platforms operate under completely different rules. Loan-to-value ratios that once reached 80-90% now typically cap at 50-60%, with many platforms pushing even lower [8]. Ledn, one of the sector's success stories, maintains LTV ratios around 50% and requires borrowers to post additional collateral if positions approach danger zones [9].

The changes run deeper than just numbers. Galaxy Research reports that over-collateralized lending now dominates the market, with many borrowers insisting their collateral be held in tri-party custody arrangements with independent custodians [10]. This represents a complete reversal from the rehypothecation = reusing customer deposits for proprietary trading that characterized the previous era.

"Detailed entity diligence and verification of assets are now standard onboarding practices," Galaxy's researchers found, contrasting sharply with the loose standards that allowed entities like Three Arrows Capital to borrow billions with minimal scrutiny [10].

But can these conservative approaches survive when markets turn euphoric again? The history of financial cycles suggests discipline erodes when profits beckon and competition intensifies.

The Transparency Imperative

Modern crypto lending platforms publish data that would have been considered trade secrets just three years ago. Proof-of-reserves reports, real-time portfolio disclosures, and third-party audits have become industry standard rather than competitive differentiators [11].

Coinbase Prime now reports quarterly loan book figures — $700 million in Q1 2024, up 75% from the previous quarter [10]. This level of disclosure was virtually nonexistent before the collapse, when platforms like Celsius marketed themselves as "safe and transparent" while operating what bankruptcy examiners later described as "Ponzi-like" schemes [12].

The technology enabling this transparency has also evolved. Discrete Log Contracts (DLCs) allow Bitcoin-native lending without requiring wrapped tokens or trusted intermediaries [13]. These cryptographic innovations enable bilateral lending agreements directly on Bitcoin's base layer, eliminating the counterparty risks that brought down centralized platforms.

"By partnering with Magnolia Financial for real-time market data, platforms like Lygos support up to $100 million in BTC collateral, offering USDC/USDT loans without wrapped tokens," according to recent analysis of institutional-grade non-custodial solutions [7].

Market Structure Transformation

The lending landscape looks fundamentally different today. Where Genesis, BlockFi, and Celsius once commanded 76% of the CeFi lending market with $26.4 billion in combined loans, today's top three players — Tether, Galaxy, and Ledn — hold 89% market share with just $9.9 billion [10].

This concentration might seem concerning, but it reflects a maturation process. The current leaders survived the 2022 crisis not through luck but through conservative risk management that limited their exposure to toxic counterparties.

DeFi lending has shown even stronger recovery dynamics. On-chain lending applications grew 959% from their bear market bottom of $1.8 billion to $19.1 billion by Q4 2024 [10]. This growth reflects the inherent advantages of transparent, algorithmic lending protocols over opaque centralized systems.

"DeFi borrowing has experienced a stronger recovery than that of CeFi lending," Galaxy Research notes. "This can be attributed to the permissionless nature of blockchain-based applications and the survival of lending applications through the bear market chaos that felled major CeFi lenders" [10].

The question investors should ask: Does this concentration create new systemic risks, or does it reflect appropriate market selection for competent operators?

Regulatory Compliance as Competitive Advantage

The regulatory response to 2022's chaos has reshaped competitive dynamics. The SEC's rescission of Staff Accounting Bulletin 121 through SAB-122 removed requirements for banks to carry client digital assets on their balance sheets, opening doors for traditional financial institutions [14].

Cantor Fitzgerald announced plans to launch a Bitcoin financing business, signaling broader Wall Street acceptance of crypto lending as a legitimate financial service [15]. This institutional entry brings deep capital resources and established risk management frameworks to a sector that previously operated on the financial system's periphery.

But regulatory clarity comes with compliance costs that favor larger, well-capitalized operators. Smaller platforms face mounting pressure to either scale up or exit, accelerating industry consolidation.

The Human Element

Beyond the statistics and structural changes lies a more fundamental shift in market behavior. The current lending market consists primarily of institutional investors and long-term holders seeking liquidity without triggering tax events, rather than retail speculators chasing yield [16].

"Their motivations now center around liquidity access, tax optimization or diversification, not yield farming," according to CoinMarketCap's Alice Liu. "This reduced the pressure for products to compete on better terms; instead, security and risk assessment have been placed at the forefront" [17].

This behavioral change may prove more important than any technological innovation. When customers prioritize safety over yield, platforms can maintain conservative lending standards without losing market share to more aggressive competitors.

Technology Innovation Under Pressure

The crisis accelerated technological development in ways that prosperity never could. Non-custodial lending protocols using multi-signature custody and smart contract automation now handle billions in loans without requiring customers to surrender asset control [18].

Real-time monitoring systems track collateral values and automatically trigger margin calls when positions approach liquidation thresholds. These systems respond faster than human operators and can't be overridden by relationship managers seeking to preserve client relationships.

AI-powered risk assessment tools analyze on-chain behavior patterns to identify potential defaults before they occur. Platforms like Wildcat and 3Jane are building specialized infrastructure that combines traditional credit analysis with blockchain-native data sources [10].

Institutional Adoption Accelerates

Traditional finance's entry into crypto lending represents more than just market expansion — it brings established risk management cultures and regulatory oversight that crypto-native platforms often lacked.

Prime brokers now offer Bitcoin ETF lending, allowing institutional investors to earn yield on their digital asset holdings through regulated channels [19]. This development creates alternatives to crypto-native platforms while establishing benchmark standards for risk management and customer protection.

"With barriers to entry now significantly reduced, institutions have a clearer path to build and expand digital asset offerings," according to Chainalysis analysis of recent regulatory developments [20].

But does institutional participation sanitize crypto lending's inherent risks, or does it simply distribute those risks more widely through the financial system?

Current Market Dynamics

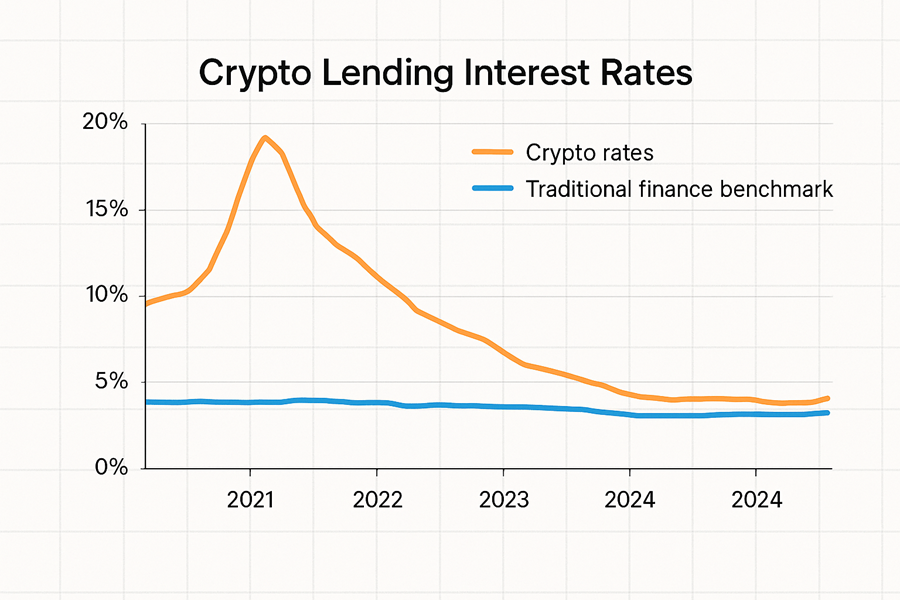

Interest rates in crypto lending markets now track more closely with traditional finance metrics, reflecting the sector's integration with broader capital markets. USDC lending rates currently range from 5-8% annually, down from double-digit yields that were common during the speculative peak [21].

This rate normalization reflects both increased competition and more realistic risk pricing. Platforms can no longer attract deposits by offering unsustainable yields backed by leveraged trading strategies.

Bitcoin lending has shown particular resilience, with institutional demand driving loan book growth of 112% in 2024 according to some estimates [22]. This growth comes from borrowers seeking to maintain Bitcoin exposure while accessing fiat liquidity, rather than speculative leverage strategies.

Remaining Vulnerabilities

Even reformed lending platforms face structural challenges that no amount of risk management can completely eliminate. Bitcoin's volatility means a 20% price drop can still trigger mass liquidations despite conservative LTV ratios [17].

Market concentration creates new systemic risks. If one of today's dominant platforms faces crisis, the limited number of alternatives could struggle to absorb displaced lending activity.

"BTC remains volatile, where a 20% price drop can still cause mass liquidations despite the platform actively monitoring LTV and enforcing real-time margin calls," Liu warns [17].

The interconnectedness of crypto markets also means contagion risks persist. A crisis in one major platform or asset could still cascade through the lending ecosystem, regardless of individual platform safety measures.

Looking Forward

The crypto lending market's recovery reflects genuine structural improvements rather than mere cyclical bounce-back. Platforms now operate with capital reserves, risk management systems, and regulatory oversight that would have prevented many 2022 failures.

But the ultimate test lies ahead. When the next bull market arrives and speculative fever returns, will these reformed platforms maintain their discipline? History suggests that financial booms erode conservative practices as competition intensifies and profits beckon.

The lending platforms rebuilding trust today face a damn tough balancing act: demonstrating they've learned from past failures while positioning for future growth. Their success or failure will determine whether crypto lending becomes a mature financial service or remains a cautionary tale about the perils of financial innovation.

The $36.5 billion question is whether this recovery represents genuine progress or simply the calm before the next storm. For investors considering crypto lending platforms today, the answer may depend less on the platforms' current policies than on their ability to maintain those policies when market conditions make them expensive to enforce.

References

[1] Galaxy Research - "The State of Crypto Lending and Borrowing" - April 14, 2025

[2] CoinDesk - "After 2022's Bust, Scars Are Healing In Crypto Lending" - August 21, 2024

[3] Cointelegraph - "Bitcoin loans are back, rewriting the book Celsius burned" - June 27, 2025

[4] Time - "Crypto Lender BlockFi Goes Bankrupt in Aftermath of FTX Meltdown" - November 28, 2022

[5] NPR - "BlockFi declares bankruptcy in aftershock of FTX's collapse" - November 28, 2022

[6] Jenner & Block - "Celsius Final Report" - 2023

[7] AInvest - "Non-Custodial Bitcoin Lending and the Rebuilding of Trust in Crypto Credit Markets" - August 29, 2025

[8] CoinDesk - "Crypto for Advisors: Is Bitcoin Lending Back?" - October 1, 2025

[9] AInvest - "Bitcoin Lenders Rebuild Trust With Stricter Controls, Loan Book Grows 112%" - June 27, 2025

[10] Galaxy Research - "The State of Crypto Lending and Borrowing" - April 14, 2025

[11] Financial Content Markets - "Institutional Crypto Loan Market Roars Back" - October 2, 2025

[12] Jenner & Block - "Celsius Final Report" - 2023

[13] CoinDesk - "Lygos Aims to Banish Ghosts of Crypto Lending Collapse With Non-Custodial Bitcoin Model" - August 27, 2025

[14] Chainalysis - "U.S. Regulators Give Banks the Green Light for Digital Asset Activities" - May 8, 2025

[15] Cantor Fitzgerald - "Cantor Fitzgerald to Launch Bitcoin Financing Business" - 2024

[16] Yahoo Finance - "After 2022's Bust, Scars Are Healing In Crypto Lending" - August 21, 2024

[17] Cointelegraph - "Bitcoin loans are back, rewriting the book Celsius burned" - June 27, 2025

[18] Brown Rudnick - "Bitcoin Lending Facility Agreements: The HODLER's Path to Fiat Liquidity" - 2024

[19] Datos Insights - "Bitcoin Institutional Adoption: How U.S. Regulatory Clarity Unlocks $3 Trillion" - July 28, 2025

[20] Chainalysis - "U.S. Regulators Give Banks the Green Light for Digital Asset Activities" - May 8, 2025

[21] CoinDesk - "Crypto for Advisors: Is Bitcoin Lending Back?" - October 1, 2025

[22] AInvest - "Bitcoin Lenders Rebuild Trust With Stricter Controls, Loan Book Grows 112%" - June 27, 2025

[23] BitNewsBot - "Best Cryptocurrency Lending Platforms" - 2024