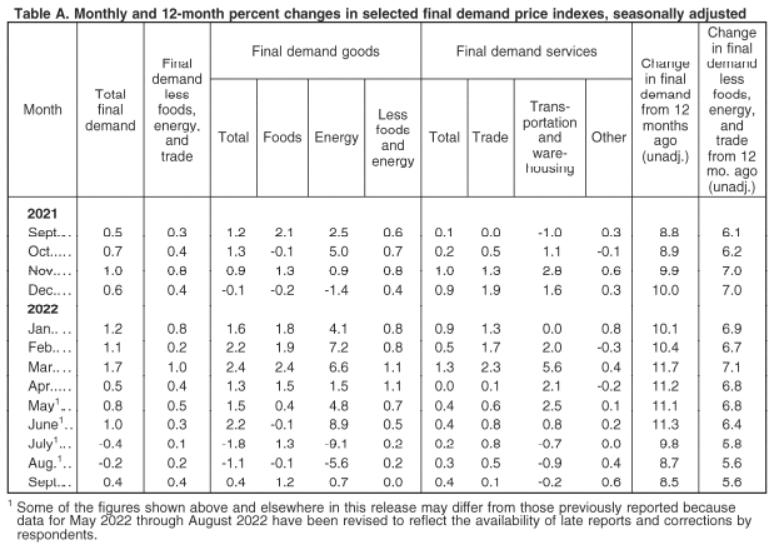

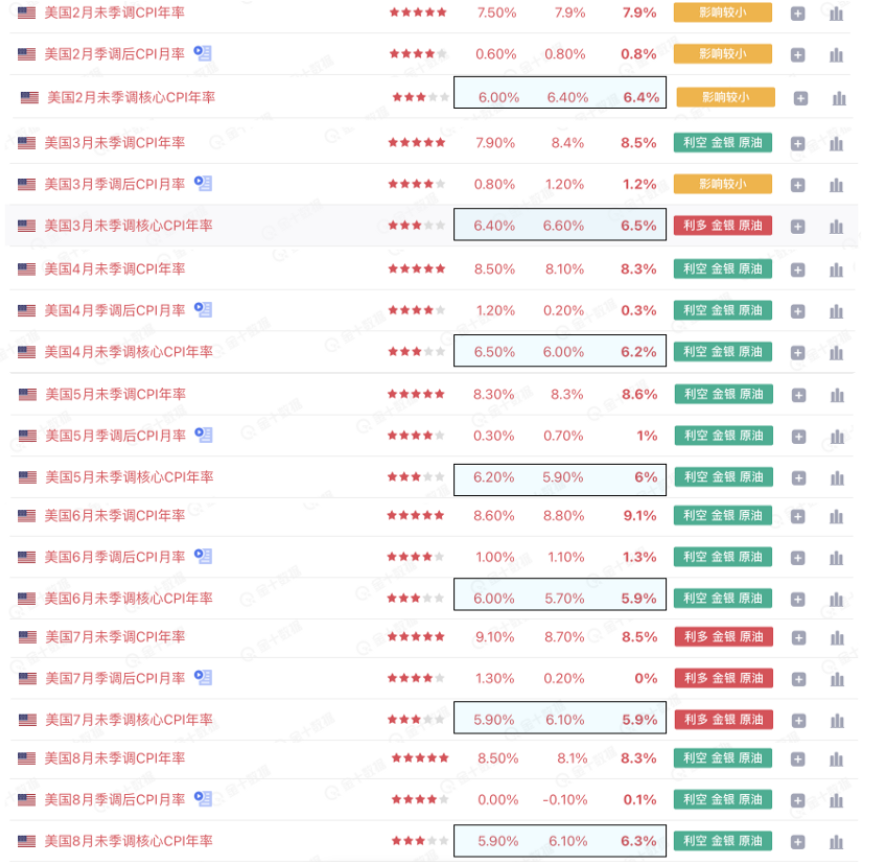

There are about ten hours to go before the release of the September CPI. In fact, the content of this CPI was already very detailed in yesterday's tweet and last night's video. Considering that some small friends may not have watched the video, today's tweets just filter out the key points. First, there is the prediction of the CPI. Last month's CPI was 8.3%, the Labor Department's was 8.1%, and the third party's was 8.2%.

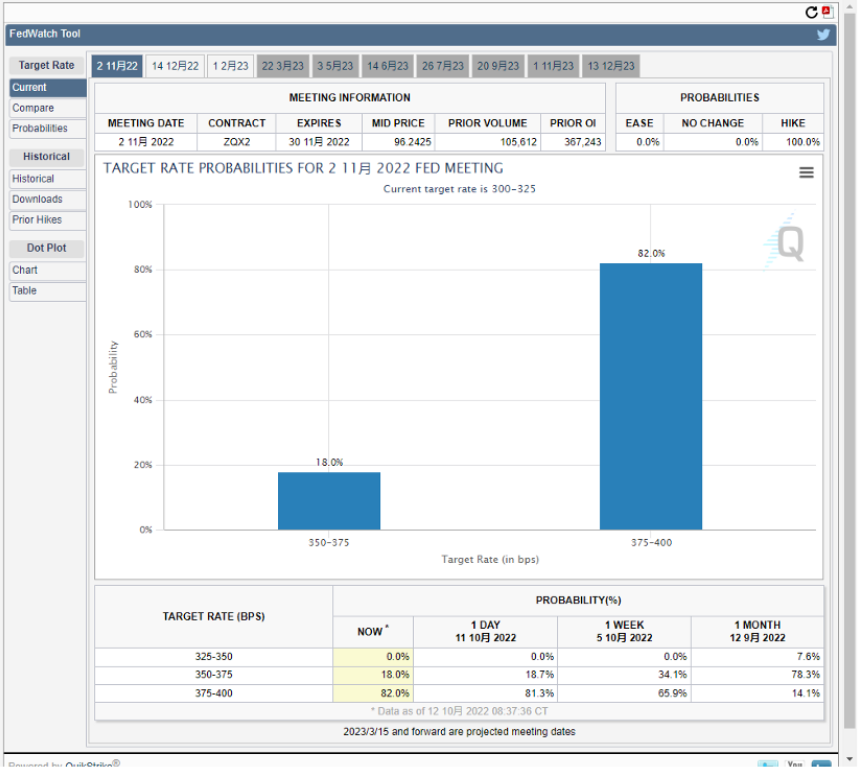

The forecasts are pretty much the same, but I've still compiled the Fed's expectations - and the results - of all rate hikes since March. It's clear from the data that the broad CPI's (pink) forecast is, in addition to once being equal to, and once more greater than, the last five months have all been when the forecast was less than, and the overall difference was around 0.3%, while all of that adds up to plus-0.3%. That means that the broad CPI reading from the Labor Department is 8.1%. If there are no exceptions, the final reported September CPI reading will be between 7.8% (-0.3%) and 8.4% (+0.3%), and the figure is likely to trigger interest-rate debate about 8.4%, because August's CPI was only 8.3%. If the reading is 8.4%, the market will surely wonder whether the Fed will choose to raise interest rates further, from 75 basis points to 100 basis points. While it is possible to see the Fed's preparedness for an inflationary quagmire alone, the impact of 100 basis points on external factors, including the likelihood of a hard landing for the US economy, the exchange rates and government bonds of partner countries, the state of the American people and the deficit at the US Treasury, is not simply a matter of adding another 25 basis points, even if a 100% increase in interest rates is not enough to fix inflation.

So a 100 basis point rise in interest rates for inflation of just 8.4% may be talked about, or even banished, by the Fed, but the odds of a 100 are still lower than the 75, who would rather have two 75s than a 100+50 shock to the market. So the maximum limit for a November rate hike would still be 75 in normal circumstances, unless inflation continues to rise, not just above 8.4%, but well above 8.4% before the Fed is likely to use the 100.

So if the CPI is below 7.8% in September, then it is highly unlikely that the Fed will choose to raise rates by 50 basis points in lieu of 75 basis points. For the Fed, this is October, and September's data are already out of date. October's PPI data, released last night on current trends, are enough to alert the Fed to the fact that the increase in production costs will inevitably translate into purchase costs.

In particular, the data released by the U.S. Department of Labor show that the trend of rising costs is basically seen in industries with a higher impact on inflation. This represents a very bad inflationary situation in October. Even if the data for September were a continuation of the downward trend, it is difficult to guarantee that October will not rebound. Food, energy and services are in particular showing a rising trend. Meanwhile, the impairment of housing and rental is not obvious. What is more troublesome is oil.

Although oil has been falling for three consecutive days, prices are still above the average for September, and the reason why prices have fallen is because the Biden administration has cooled the market by releasing strategic reserves. This is not to say that palliatives are not permanent. Even palliatives are not counted. With the Fed tightening and the Democratic tapering, understandably, votes count for more than anything. So the rest of the month is about whether oil prices can fall further. So given the various indications that inflation in October may be getting worse, even if the Fed sees signs that inflation eased in September, it will not dare to raise interest rates by 50 basis points to stimulate the market. Once the risky markets are reversed, not only will inflation rise, but even if the Democratic Party sends a signal that oil prices will drop and go back up, so the Fed will not give the market such a "wrong" indication. So, regardless of the rise or fall in the generalized CPI, as long as it remains within the +-0.3% range predicted, the Fed will not reverse its decision to raise interest rates by 75 basis points in November. The Black Swan, after all, has a small chance that if it happens, the White House will be able to deliver a pre-emptive statement before the CPI is released tonight, but not if it does. Another is whether the movement of the core CPI will influence the Fed's decision to raise interest rates.

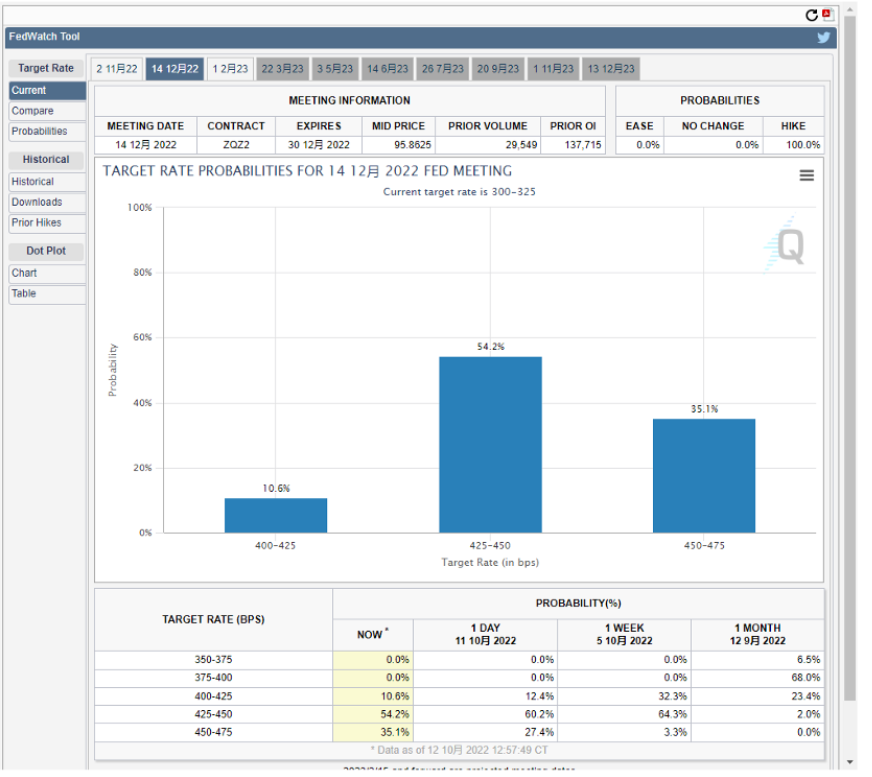

Back to the forecast data can be seen that the core CPI (blue) expectations and published value gap is smaller than the generalized CPI, basically the difference is +-0.2%, and compared to the generalized CPI overestimate and underestimate are likely to appear. So if you add the difference to the forecast, the Labor Department's forecast is 6.5%, and the core Consumer Price Index for August is 6.3%, so we know very well. Under normal circumstances, the range of the core CPI announced tonight would be between 6.3% and 6.7%, which means that the best case scenario for the core CPI is predicted to be equal to August's data, while one would expect the core CPI to be higher than August's. Thus, even if there were an impact on the Fed's rate hike, one could rule out the possibility of a 50-basis-point increase, while the more likely scenario is between 75 basis points and 100 basis points. The question then goes back to the broad CPI that came before. It is still highly unlikely that the Fed will raise interest rates by 100 basis points because it is already 0.2% higher. Therefore, through "seeking swords," we can arrive at a high probability and accurate data that no matter what the general CPI and core CPI are up or down, as long as they are within the range of prediction, there will be no interference in the Fed's policy of raising interest rates. The question then arises whether risk markets will bounce back from the CPI data, in anticipation of such an outcome, or continue to fall as a result of the CPI's poor performance, knowing that it will not reverse the Fed's decision to raise interest rates by 75 basis points in November. This issue will really depend on the data released by the CPI, because although it will not affect the quota for November's interest rate increase, it will still affect the December interest rate increase and the terminal interest rate. The historical trend can be seen that if the CPI data is better than expected, the risk market will rebound on the current basis, and the extent of the rebound depends on the trend which is better than expected. But we already know from the analysis above that the probability is better than expected, and the gap will not be very big, so the height of the upward rebound in the risk market will not necessarily be too big, and will still be affected by the interest rate increase.

And if it falls short of expectations, risk markets are bound to continue falling. After all, inflation in October was already very bad, and a worse number in September would suggest that current expectations may be wrong, and that further increases are needed. The Fed's original 50-basis-point rate hike in December would most likely be derailed. A further 75-basis-point increase by then is not out of the question, but only brings the terminal interest rate to 4.75%. After two days of frequent speeches from Fed officials talking up the battle with inflation, the markets are being told that the Fed wants to push rates above 4.6% by early 2023 when there is no 4.6% increase, only 4.75% is possible. It also shows that at least the hawks are ready to raise interest rates by 75+75, and the second 75 is totally higher than the market expects. The risk markets will surely fall.

So there's no need to raise expectations too much. After all, the upside potential is really limited. If there is a downside, where is the relative bottom of the risk market? I made an expectation for Nasdaq futures, BTC and ETH, starting with Nasdaq futures. Between June 10 and June 30, 2022, Nasdaq futures fell 5.21%. Another marker is that between Sept. 13 and Oct. 3, 2022, Nasdaq futures fell 14.19%. Both ranges were chosen because they correspond to two CPI releases each time, and the 20-day gap between them is exactly 20 days from Nov. 3, when the CPI was released to the Fed, so looking at the two Nasdaq futures had 20 days of declines to guess how much this one might fall. The comparison of the data shows that if we calculate today's average price, then the Nasdaq futures would continue to fall after today's CPI announcement, and fall another 20 days, and 15%, by November 3. Then they would probably fall to around 9,300. So, this figure is already back to May 2020. And if, as in the previous case, it would only fall by around 5.3%, the possible losses would be smaller, only to around 10,200. The price of BTC and ETH is highly correlated, especially if the time of the currency market is also adjusted to UTC-5 (New York time), then we can obviously see that the price of BTC futures rise and fall and the synchronization of BTC are also highly correlated, and this theory is a gage of the bottom range of BTC and ETH prices.

The BTC was also marked with two markers, at the same point in time as the Nasdaq futures, especially for the 20-day decline from Sept. 13 to Oct. 3. The Nasdaq clearly saw a 14.19% decline in the Nasdaq, versus a 14.94% decline in the BTC, with a 0.75% gap between the two, proving that the synchrony of the BTC and the Nasdaq is more than just rhetoric. It follows that the BTC's price will fall another 15% with the index futures. The final price may fall to around $16,200, but in fact it will be hard to see such a large decline because it has fallen below a new BTC low. Another marker for BTC is a 33% decline that began on June 10, but that was largely due to the loss of a lot of leverage, which has exploded a central highly leveraged platform like 3AC. That was due to the LUNA-UST nexus. It is no longer possible to do so, especially since the amount of leverage that should be cleaned up in the currency market is close, it is no longer possible to solve the problem of reducing leverage by 33%. Therefore, the BTC can be reduced by a relatively limited amount. The same is true for the ETH. Moreover, the number of profit addresses of the BTC is still higher than that of the ETH, so the selling pressure of the ETH is not necessarily heavy.

Of course, there is also data for ETH in the same coordinate, the only difference being that because the merger of the ETH on September 14 caused a more drastic change in prices, the selling pressure on the ETH would also be slightly heavier than the BTC's fall by about 25.6%, at which point the ETH would be about $960, and at about $1,100 if the BTC and Nasdaq had fallen by 15%.