"This market is too magical" at the start of two days in a row, and it's too magical today to use again, but it's too magical, and it's actually quite simple: During the US mid-term election, the Democrats can't just keep their vote-by-vote going, the economic climate is already very bad, the risk markets are falling, most Americans are living standards are falling, and inflation is continuing to be high, leading to a contraction in purchasing power.

In this case, the ruling party wants votes, either to change the economic environment and force the Fed to slow interest-rate hikes, to reduce inflation by addressing the supply-chain problem, or to spend money on "votes," which the current president undoubtedly chose. If nothing else, take oil prices. The main reason for the moment is that sanctions against Russia have raised prices in Europe and the US. It is also a mistake to blame Mr. Biden for not trying; to go to Saudi Arabia at that age would be the least face-saving way to increase oil production. Alas, just a month later, on the advice of Russia, OPEC+ began a production cut mode instead of increasing production in October. The production cut was more than twice as large as the production cut originally promised to Biden. As a result, the price of oil has risen, not fallen, into October. Oil prices are now above their September average, and are about to touch their August average. This is a major headache not only for the Democratic Party, but also for the Federal Reserve. It was also because higher oil prices erased any post-October jobs gain and a bullish mood fueled by rumors of falling rents, that investors stopped betting that the Fed would choose to raise interest rates by 50 basis points in November.

Instead, they moved on to a 75bp rise, which is why risk markets have been falling since yesterday. The market can regulate itself, but the Democratic Party, with only a month to go until the mid-term elections, has no time to adjust. As we said earlier, the first two routes are either a cure or a symptom. But one requires more time, and the other requires the Fed to put its face on it. Clearly, there is no short-term solution. There's only the last vote to buy, especially in the U.S., which is a country on wheels. Cars have to be used for travel, and oil prices are something that almost every American can't escape, so they can only delay the mood of the electorate by releasing their strategic savings of oil and selling it to the market at a low price. But strategic reserves also need to be bought with money, so that's why the Federal Reserve has asked everyone to tighten their belts, raising interest rates and shrinking their watches, to control purchasing power. The other is the Biden administration's "watering down" of votes. The result is that the two functional departments that should have come together have been estranged. The Fed's interest-rate hike is itself a boost to US Treasury spending, and Biden's vote-for-oil purchases are bound to increase the fiscal deficit. This means that subsidies will not last, and that oil prices will remain high after the mid-term elections, when CPI estimates will be even more dismal. But the problem here is not over. Although Biden has already called for using oil reserves to cool the market, as he did last time, he has only called for oil reserves, and there has been no actual purchase, so the market is happy to continue raising oil prices. Therefore, the risk market is expecting that Biden will "buy votes" to stimulate the stock market, and the oil merchants are raising oil prices because Biden has not paid for them, creating a situation in which the risk market and oil prices are both rising.

But for the risk market, as long as Biden does not pay for a day, the rise in oil prices can not be restrained, and the rise in oil prices will certainly make the expected CPI continue to go up. Therefore, relatively, the risk market is more prone to large fluctuations recently, and large fluctuations on both sides will also lead to large fluctuations in BTC and ETH prices, especially in the Q3 results starting next week. So risk markets as a whole are bound to become mired in deeper volatility, for which any one-sided bet could be costly, especially to more leveraged currency investors. Instead, it is a call or short position that is the best way for most investors (like me) who do not have sufficient confidence in their short-term trading abilities. Because as oil prices rise, expectations of higher interest rates rise.

The knock-on effects have already helped the dollar index, which was on a downward trend, to break through 112 today, and Treasury bonds, which have just added some liquidity, have resumed a large capital exit, shifting the entire market game from one between the economic wing and the Fed to one between the Fed and the Democrats. The September CPI report is only a week away from being released on the 13th, but it is no longer the main issue.

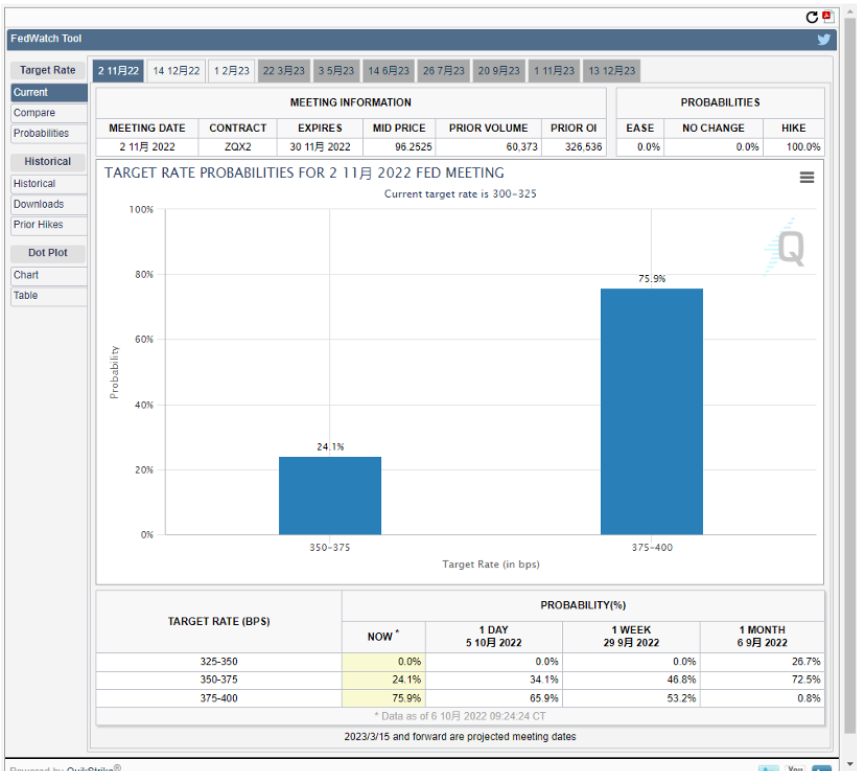

However, the unemployment rate and non-farm data to be released tonight remain the most important gages on which the Fed caps interest rate hikes. Judging from the Labor Department's current forecast, the unemployment rate will remain at 3.7%. This data probably won't hold, and the drop in the non-farm data to 25 also represents the beginning of a cooling of the labor market. Of course, this is what the Fed would like to see. Therefore, "the weakness of the employment data is a good sign for the risk market." After all, the Fed's biggest expectation of an increase in unemployment is around 4.4%, beyond which it will have to slow the possibility of rate hikes or cuts. Non-farm data is positive, which is not bad. Once non-farm data is negative, the game is expected to be the strongest, and this period is also one of the criteria for BTC and ETH to hold positions.

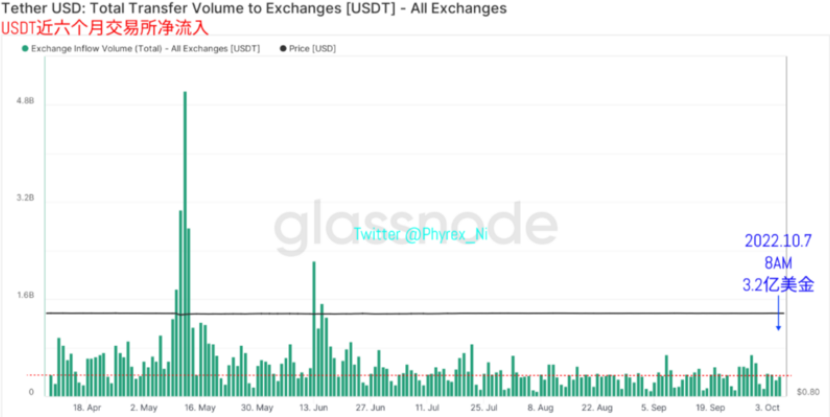

Back in currency markets, the main anchor, which itself represents the maximum purchasing-power ceiling, has been steadily declining, with expectations of CPI and the exit of money from US Treasuries increasingly reinforcing investors' determination to hold dollar cash. So as of 8 a.m. today, USDT, the main purchasing power, has bucked the trend in market value, adding $150 million, albeit not much.

However, it represents that part of the European and Asian capital has been transferred from the wait and see to the entrance, whether it has been bought is not a good way to judge, but the increase in market value will certainly enhance the maximum purchasing power limit, especially for the main force of the transaction. For the secondary major BUSD, there is no new change in market value, neither increased nor decreased, which also shows that the fee-free also can hardly continue to drive the increase in turnover.

On the other hand, USDC, the main selling group, still lived up to expectations and drove another 270 million US dollars out of the market. In the last month, USDC's market value has dropped more than 5 billion US dollars, and most of this money has really left the currency market, representing more US investors who are not optimistic about the trend of the currency market for the next period. It is also a mockery of the rapid rise in USDC's market value since the BTCETF, announced this time last year.

For more DAI used for the ETH spot leverage, the market value fluctuation is still moving towards the direction of selling. Although the price trend of ETH is not as strong as that of BTC recently, but it still follows the BTC closely. The reduction of the spot leverage shows that investors do not favor the next trend of ETH. Finally, looking at the total market value of the four stablecoins, thanks to the increase in the USDT market value, the overall market value of the stablecoins was relatively stable, with a decrease of only $140 million.

Although the overall market value of the stablecoin is not friendly, the amount of money is certain to be certain as of 8:00 a.m. this morning when the USDT is converted into purchasing power, which shows that although the risk markets are still volatile, there is no CPI in September, and even the Federal Reserve's interest rate hike is still unclear, there is still strong purchasing sentiment to "buy at the bottom" of the market, and judging from the details, it is still quite possible that the Europeans will do so.

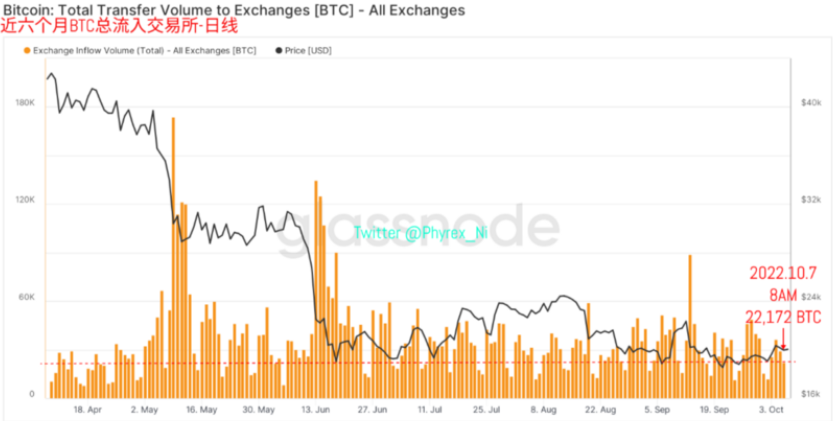

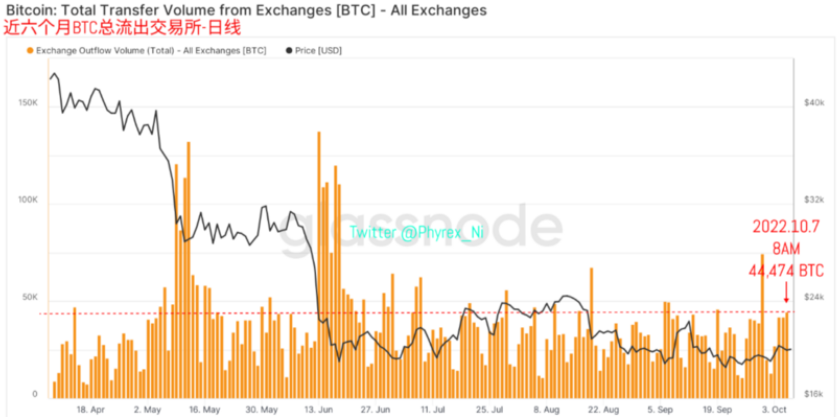

Judging from the selling pressure that BTC and ETH have transferred to exchanges, compared with the overall amount of selling pressure in the first few days of this week, there is a tendency to show a slowing tendency. On the one hand, this is because prices are relatively stable; on the other hand, this is also because after a long period of oscillation, many investors believe that now is a relative bottom. In particular, even if there are losses, they remain low and do not cause a major panic.

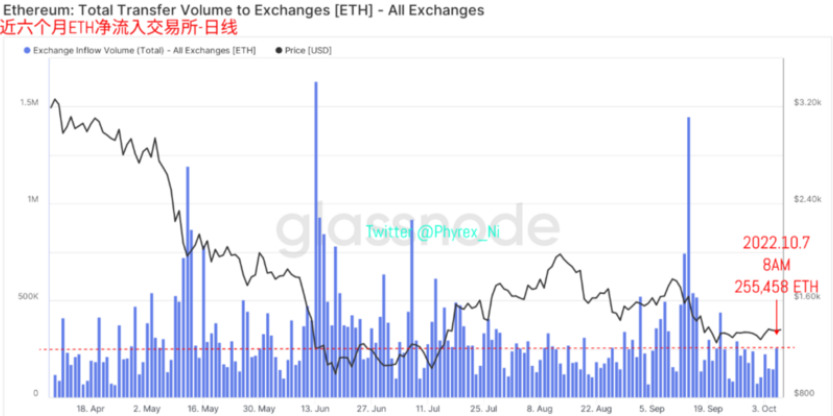

The ETH selling pressure has continued to show signs of increasing, from the details, because last night into the Gemini there were nearly 30,000 more ETH, and this has been a large number of Gemini transfers, although not very clear proof, but can be judged by the signs are likely to be the exchange of arranging wallet behavior, and not like the direct user-generated selling pressure, so the impact on price is not great.

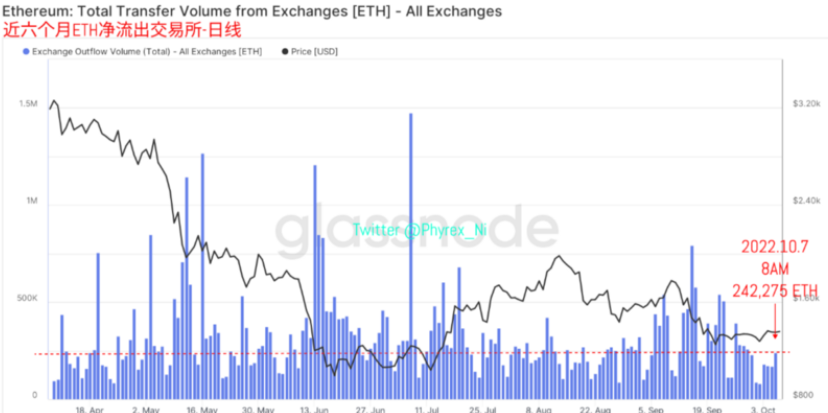

Compared to selling pressure, from the exchange transfer cash withdrawal data, both the BTC and ETH withdrawals have increased in various ways, and there is no downward trend due to the changes in the mood of the risk market. This also shows that the purchasing power of users is still above a certain level. Of course, it is more important to look at the CPI data due to be released next week. Moreover, from the detail data, Europe is still the main buying time.

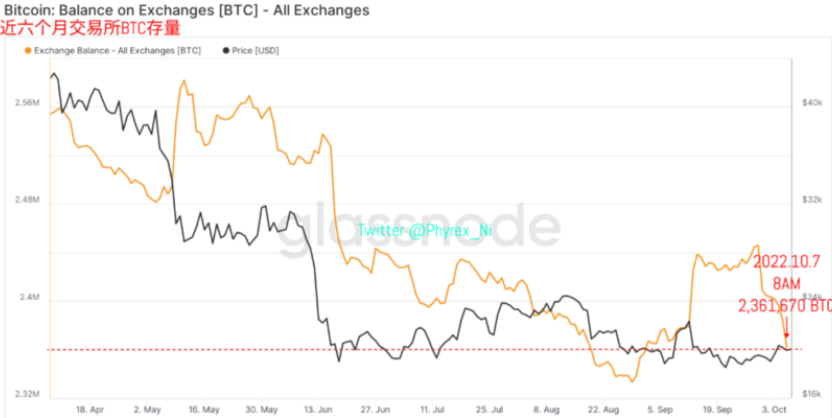

The stock of BTC can also be found through the stock of ETH, although the stock of BTC has not broken through the new low, but it is not far away from the low point of nearly three years, and there is a chance to achieve this, which shows that the stock of BTC is in a strong buying mood, while the stock of ETH is still in a high position. While there is a possibility of intra-exchange leverage, the high stock levels create uncertain risks.

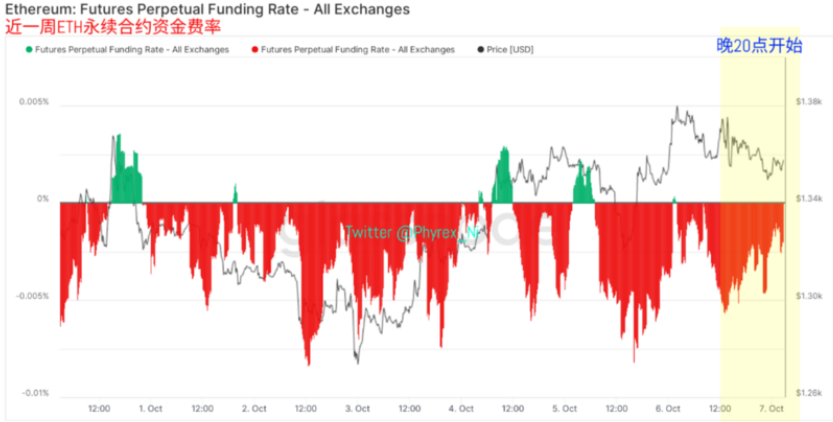

From the emotional point of view, the current BTC and ETH are moving in two different directions. BTC itself is a strong bullish sentiment, so it remains bullish. In contrast, although the price of ETH is also good, but bearish is dominant, and it is also a large area of bearish. In the face of the more complex market game behavior, unilateral long-short is dangerous.

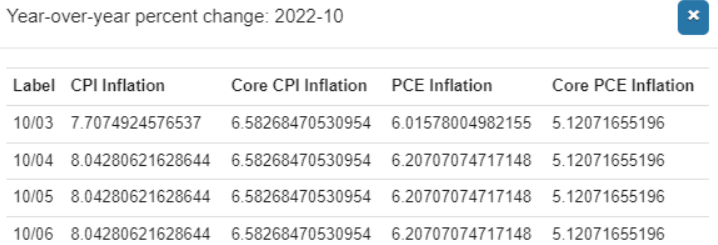

To sum up, the current macro sentiment is still very delicate and full of various uncertainties, but generally speaking, the conclusion of November interest rate increase will not be known until after the release of the September CPI. But if the price of rent decline does not reflect the September CPI, from now on, the probability of CPI inversion in October is not low, which should be a good opportunity for our small partners who are preparing to take the bottom of the BTC and ETH. The instability of the Nasdaq futures also shows the intensity of the game. Moreover, the BTC and the ETH may not survive the change of the big trend.