Current Summary:

Capital is always the best judgment of whether the market is strong or weak, whether in stock, currency, or even bond markets. And what affects capital more often is macro-level adjustments, because capital is profitable. Where there are relatively stable returns, more capital will go. But something has changed recently, and that's because there are a lot of things that we don't yet know.

The dollar index, known as the US dollar index, has been rising through the current bear market because of changes in macro conditions such as interest-rate rises and contraction, hitting a high of 109, the highest level since June 2002, and representing a greater willingness of investors to hold dollar cash or dollar equivalent assets such as Treasuries than venture capital, especially as Treasuries are more popular in bear markets.

In the first and second quarters of this year, the US Treasury's colonial rate moves were highly correlated with the macro picture and were essentially the best response to the rate increase, but the market has responded differently since the weekend. The first is that the exit of a lot of capital has led to a sharp rise in yields in the bond market, with short-term yields peaking around 3.2% and medium-term yields averaging above 2.8%, especially the one-year US Treasury yield almost reaching its recent peak.

On 14 and 15 June this year, although there were also historical highs, there were quickly massive fund purchases that brought down the yield, which was also in line with the normal flow of funds in the market, and this time, although there was no June 15 high, nor was there much difference, there has been no clear downward trend for three days, which means that part of the market, or even the larger part of the market, does not want to enter the US bond market.

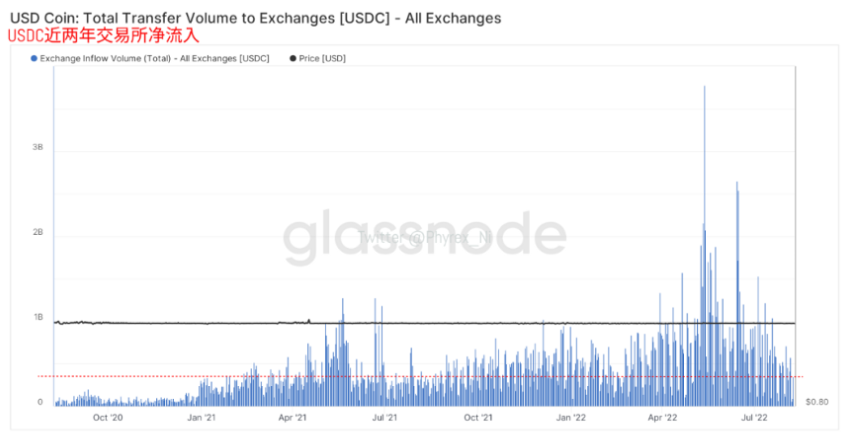

As I've said before, capital is for profit, and especially in a bear market, it's low-risk, high-stability products that are the focus of investment, so Treasuries have been the best target in a bear market. And this withdrawal of funds from the bond market and more bystander funds do not necessarily represent an opportunity for the risk market, because as things stand, even gold does not carry such a large amount of funds, and from an investment perspective, this is not necessarily a bad thing. Money is more transparent in money than in opaque markets, especially in stable currencies, which are the best measure of capital entry. While the withdrawal of a large amount of money from the U.S. debt did provide access to risky markets, there is no clear sign yet of entry into the currency market, with the USDT continuing to increase in small amounts and the USDC almost to decrease in equal amounts, and this is more likely to be a currency move.

Although we have previously analyzed that there is enough money in the money community to push the BTC and ETH to their 2021 highs, more money is not willing to enter the market in the absence of clarity, and the stimulus of outside money is a signal of whether the market will turn, which, alas, has not yet emerged. That is also the reason that there is not enough money, not enough purchasing power.

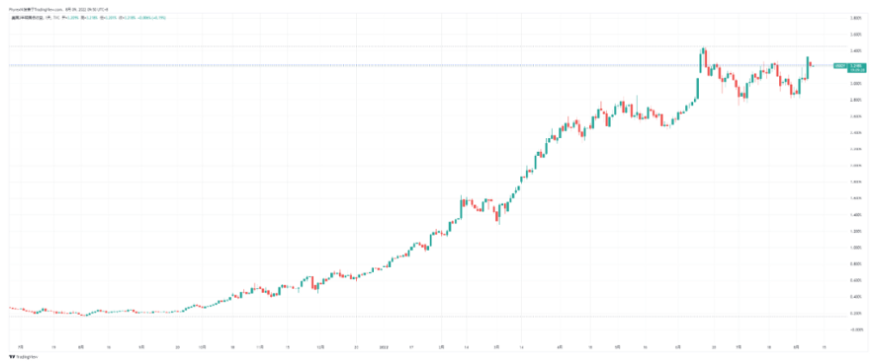

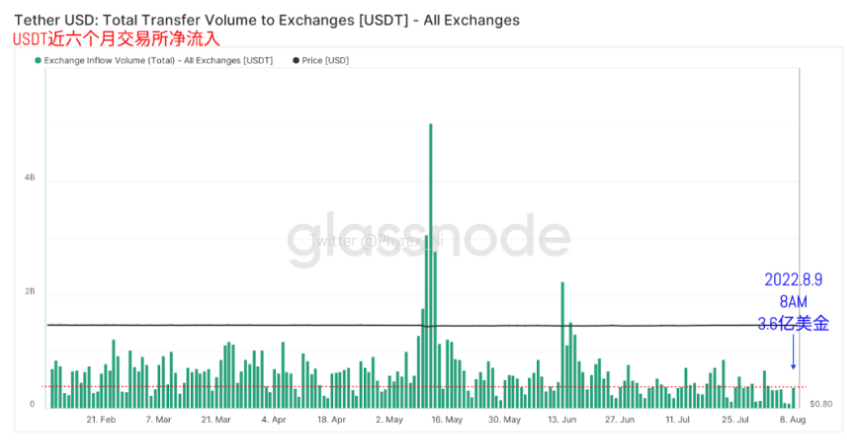

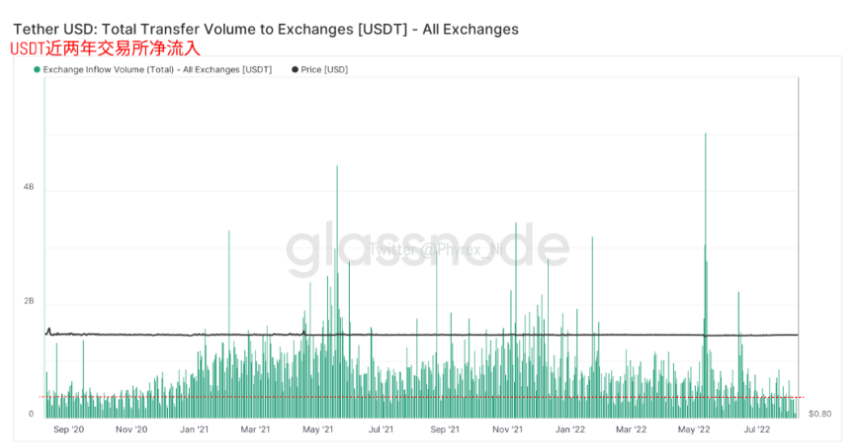

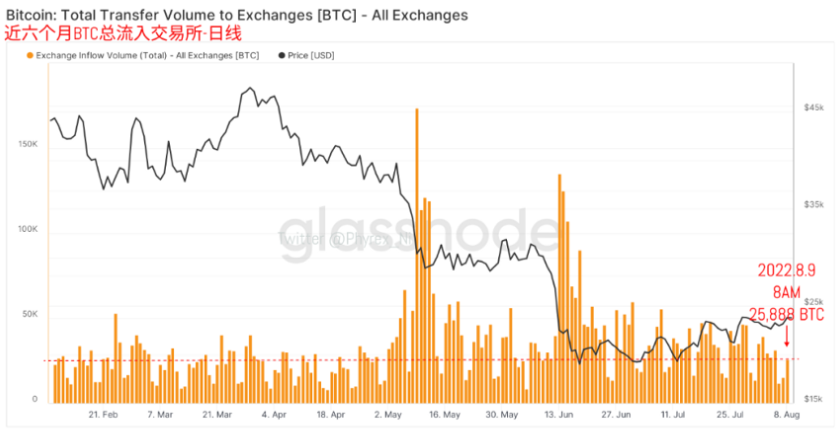

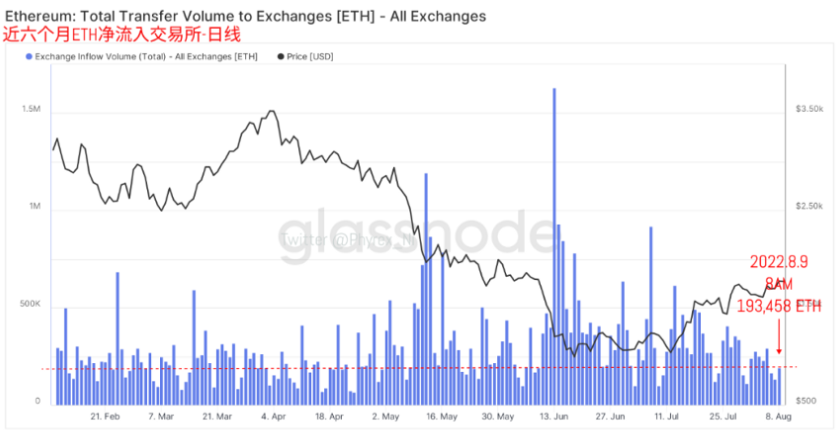

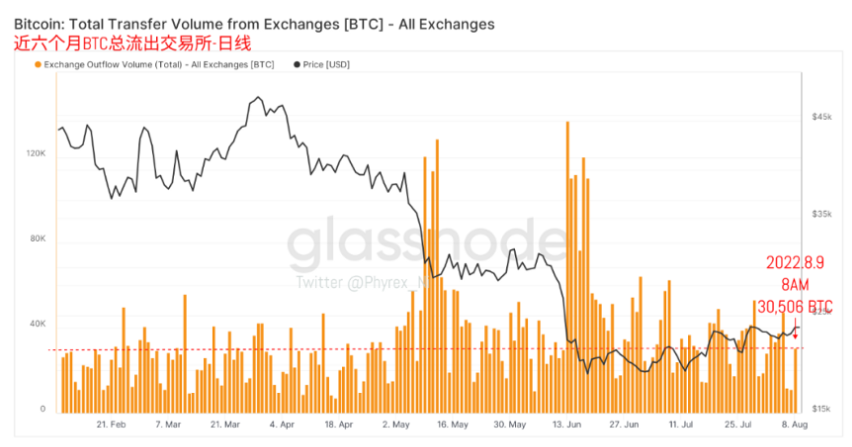

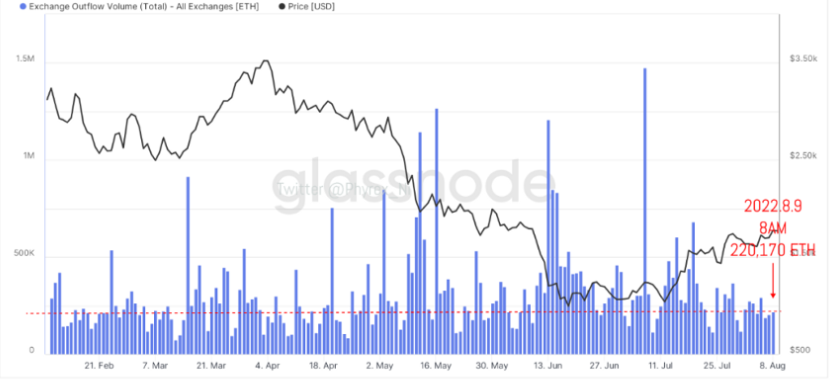

When purchasing power is in a low state, large-scale price increases and even a shift in trends are completely impossible. According to the USDT data of purchasing main forces as of 8:00 this morning, last Wednesday, 45 May, last week was the lowest amount of money transferred to the exchange in the last six months. But today's data, although a small increase, are still unable to get out of the lowest range. Compare the data from the last two years to today's levels of funding. And don't compare it to the high of prices in 2021 or when BTC and ETH prices began to fall in the first half of 2022. Even in the fourth quarter of 2020, the BTC was still around $10,000, and the ETH was spending more than it is now in the $300-plus range. They also illustrate the gap in purchasing sentiment towards the market.

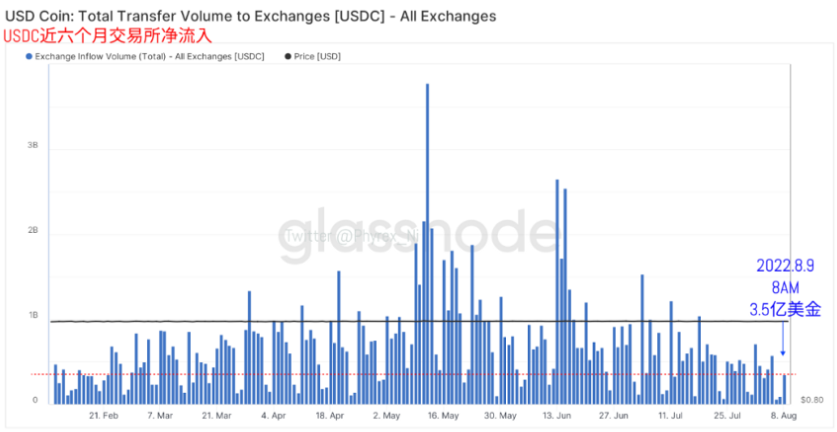

The low tide for USDT represents the view of the market as a whole, so even USDC will not do better, and USDC data as of 8am this morning were barely bigger than the amounts available on Thursday and Friday, barely above the minimum on Wednesday. Although USDC compliance has led to a flood of money as digital currencies have gained mainstream acceptance in the US, it is still only equivalent to purchasing power in early 2021.

The decline in capital, though limited purchasing power, is likely to remain at the current level of purchasing power in a downward phase, so there is no need to see that both the BTC and the ETH are now in a downward trend, not to mention that as the CPI data release on Wednesday approached, more chips are being put on the exchange, not to sell right away, but to prepare for a preventive situation.

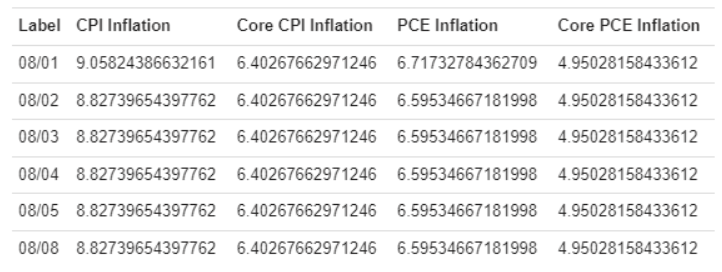

Judging from current forecasts, although the July CPI that will be released on Wednesday has a chance of being lowered, after all, the price of oil has dropped from above $110 in June to about $100, core inflation such as business and services has not declined, which has created a tense atmosphere for the data game, and whether inflation has peaked represents not only the face of the current US president, but also whether it represents the "bottom" of the chip in July. It is hard to predict directly whether inflation will fall in the current forecast, which was 8.9% last month and 9.1%. This month's forecast is still at 8.9%. This makes it hard to say why, but it is clear that a peak in inflation can at least be defined on a phased basis if the CPI numbers decline on the quarter-on-quarter basis, and that the Fed's ad hoc meetings are less likely. After all, the strong non-agricultural data have given the Federal Reserve the basis that the US economy has not yet contracted, and if the inflation situation in August does not get better, given the economic situation, the possibility of the Federal Reserve holding an interim interest rate increase meeting cannot be ruled out. And that's where risk markets face even more painful choices.

Although none of the data above is exactly favorable to the risk market situation, in fact, just because the size of the currency market is small, it actually gives the currency market an opportunity to develop, especially in the 2022 bears without any doubt, in the midst of a negative macro situation, the only foreseeable advantage is the ETH merger, no matter how the POW and POS debate, can not be denied the merger gives ETH greater enthusiasm and room for speculation. Also driven by the favorable ETH merger, in the case of narrow price volatility, the circulation of BTC and ETH reduced, more bottom-buying chips because of the expected date, so no frequent short-term operation, the maximum is the transfer of chips to the exchange ready to leave the market at any time, but as long as the price did not fall below the threshold, then these chips have enough patience to wait for the merger to occur. That is why even small amounts of money in a currency market can pull the trigger, as they do at weekends. It's hard to see a small amount of chips falling, but a small amount of money pulling remains. From exchange turnover you can see that with the falling of the pressure, the volume also gradually reduced. The CPI data is important for risk markets, but it will be better for the current currency market, if not more. After all, the next stock-market rally will wait until the third-quarter earnings report is released in October, and as the current macro picture shows, even the top companies are starting to see job cuts, not to mention other companies. The money market itself has little positive information, with the expected BTC spot ETFs still far off and perhaps not even in the entire bear market, and the likelihood that the epic event of the second-largest ETH by market capitalization will trigger an independent movement is not low.

As can be seen from the stock of the BTC and ETH exchanges, BTC that has continued to move out of its minimum stock for nearly three years needless to say, the price of narrow swing is not very profitable in itself, so the selling pressure itself is low and healthy. And while ETH, which has risen too fast, has a lot of money to gain, sentiment has remained high, including split air drops, as high turnover rates and the expected timing of the merger continue