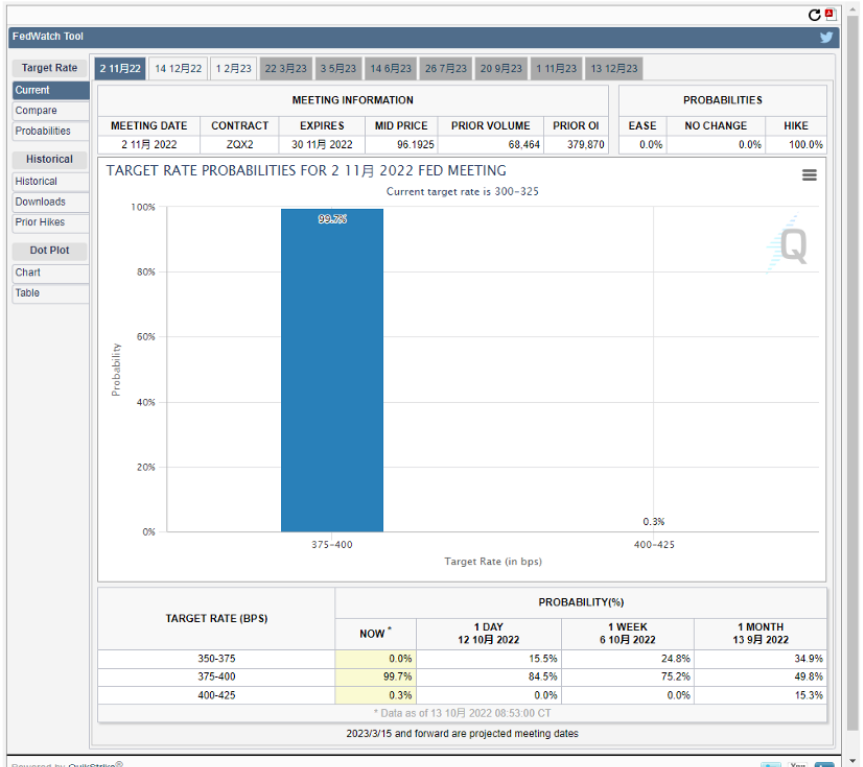

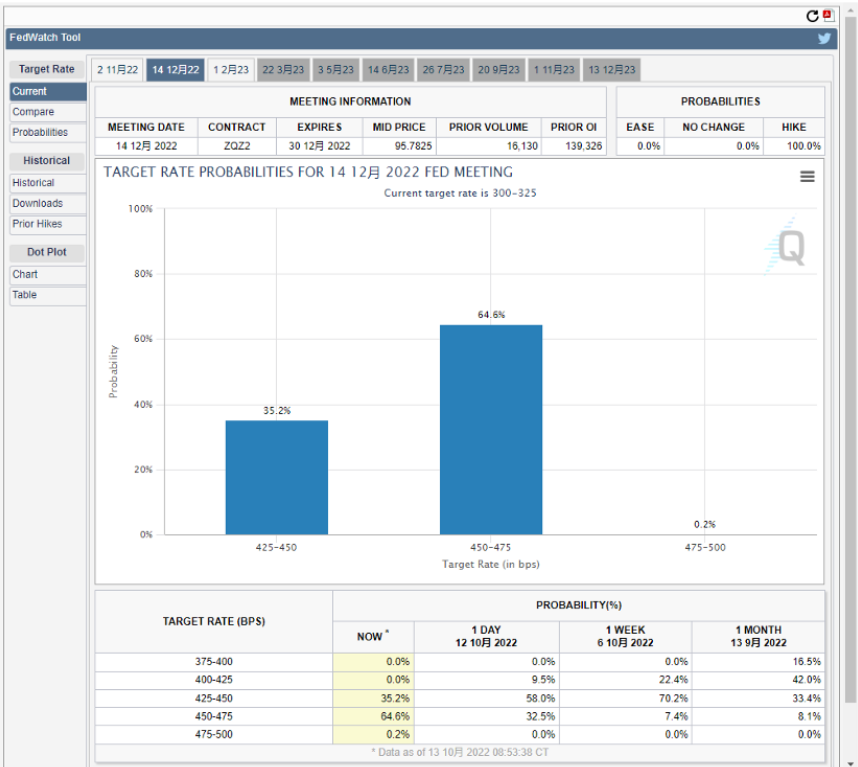

The world is truly magical. This should have been the third time, but it was magical enough. Although yesterday evening's broad and core CPI beat expectations by only 0.1%, the better than expected result was a fall, no doubt about it. First fear of a 100 basis point rate hike on November 3, and then fear of a worse CPI in October, leading to another 75 basis point or more rate hike in December. But the magic is in that when markets gyrate wildly downward, Nick, the Fed's mouthpiece, tweeted that apart from the mostly healthcare inflation spike, three more tweets - the first about the Fed's determination to hike interest rates by 75 basis points in November - looked bearish, but in fact shot down the odds that many thought the Fed would go for a 100 basis point hike. It went from bearish to bullish. While that didn't change risk markets, the next tweet not only cooled them down, but also drove home the message that the Fed doesn't really do anything about inflation. In other words, the Fed doesn't think that consistently high rates are the main reason to be fighting inflation, and Nick's Tom Waller, who was on the Fed board at the November meeting, was keen to talk about a December rate hike of 50 basis points.

The last tweet, while adding that Chicago Fed Chairman Evans had already signaled last Monday that inflation will not be fully inflation-proof for a "disappointing" rate hike at a breakneck pace, also set the tone for the last one, where the Fed may not be under enough pressure to support a rate hike of more than 125 basis points in the next two moves - that is, a 75-point rate hike in November and a 50-point rate hike in December are already a compromise - and upward resistance could be strong.

It was also because of these three tweets that risk markets began to move gradually from the bottom, and led the Nasdaq futures from a trough of a sharp decline of 3.6% to a peak of more than 2.2%, completing the magic of the CPI. So it is not hard to see that the Fed is indeed a master of expectations management. As yesterday's video suggests, even a big rate hike would have made a very different difference under different interpretations.

But whether that trend can be extended, especially if tomorrow is Friday, the last working day of the week, and what happens to prices will weigh on the mood the following week. There is no clear answer, but there is a reference that tells us what the market will do tomorrow: the dollar index. The DXY is more sensitive to rate rises than the Nasdaq futures, and is more sensitive to moves in its chart.

In other words, if we find that the dollar index has not fallen, but has also risen significantly, it means that the market thinks that the Fed will intensify its efforts to raise interest rates. And the DXY will react faster than the DXY futures. Therefore, it does have a certain effect to determine whether the rise of the DXY futures is a "hoax" through the dollar index. And the rises and falls of BTC and ETH are still in a relatively high consistency with the DXY futures.

Another indicator to watch is gold, which has been talked about before. Compared to BTCs and ETHs, gold's price performance is not as indicative as that of the index futures, nor is it forward-looking as the dollar index. But gold's continued decline suggests investors are scarcely willing to put their money into anything other than dollars, and that sentiment has not returned, with dollar holdings the dominant currency. So the situation is clearer now that the game has shifted from the 75 or 100 points rate increase in November to the CPI in October and the rate increase in December. For investors, the big change in sentiment is first and foremost a Fed rate hike on November 3, but the suspense is almost over. By then, a 75 basis point landing would be expected to be bad news for risk markets, and it is not hard to imagine a rebound. The second key to macro sentiment was the US October CPI data released at 20:30 p.m. on November 10. Although it is already known that the Federal Reserve will most likely choose to raise interest rates by 50 basis points in December, this assumes that the CPI data is not excessively high, for example, that more than 9.1% will break the record high, even though it is relatively unreasonable, and if this happens, it is not yet known whether the Fed will abandon the 50-point rate hike and increase the rate. But the odds are not going to be low. And when that happens, it means that all the Fed's actions from March, when it began raising interest rates, to now, are meaningless, dragging down the US economy, bringing down allied markets, increasing massive Treasury deficits, making US debt less liquid, and even increasing US unemployment, in exchange for higher inflation rather than lower it. This is not what the Fed wants. The last two big macro-sentiment effects of the year were the US CPI for November, which was released on December 13, and the last interest-rate hike of 2022, which was released at 3:00 a.m. on December 15. On the contrary, the last two major macro-sentiment effects were small compared to what had been expected before. So the chances are that in 20 days, there will be a slight uptick, and that in a week's time it will be the last game of the year. All of this is really meant to sum up the bottom of the risk market in two phases. The first is the 20 days remaining before Nov. 3. As results of leading technology stocks emerge, and we already know that several stocks, including Meta, may not fulfill our expectations for Q3, there is a real risk that the Nasdaq will fall during this time, and to what extent that represents a bottom in the hierarchy.

But it is only a bottoming out of phases. The trend of financial reports may not last long. It is more about changes in the broader environment. Therefore, whether risk markets, including BTC and ETH, will further bottom out or not depends on the CPI in October and the Fed's statement when it raises interest rates in November. If the CPI in December is higher than 50 or lower than 50, risk markets will surely continue to bottom out while the latter proves that it has already been a bottoming out. And to be clear, even if a relative bottom is certain, the Fed's rate hike is still a long way from the bulls that many of its junior partners expected. Given that the Fed's interest-rate hike is intended, even if it does not lower inflation, to buy the White House more time to reduce supply-side costs through political means, there is a very good chance that the Fed will not choose to cut rates before inflation reaches a certain level, but will instead keep its terminal rate at roughly 4.5%.

Moreover, the bull market is not without reference indicators, U.S. debt can be used as a reference for the bear-bull conversion. Only when the yield on U.S. debt decreases and more funds are no longer able to obtain higher returns on U.S. debt, will there be more funds gradually transferred from the dollar market to the risk market, and there will be a chance to start a new round of growth. At the moment, only one-month Treasuries are worth more.

Another indicator that can be seen directly from the currency market is the total market value of the stable currency. After all, the market value of the stable currency is the benchmark for measuring maximum purchasing power, and the yardstick for measuring external funds' confidence in the currency market to recover. As of 8:00 a.m. today, the total market value of the four major stablecoins continues to show a downward trend, and they have lost over $240 million, a significant recent decline, but it still needs to be analyzed in detail.

The first visible change in the market capitalization of USDT and BUSD, the main and secondary trading forces, is good news if it does not decline, but it also shows that even though there was a relatively large drop yesterday, which may indicate further falls to come, there is no sign of capital coming in, which shows that even if we are ready to buy at the bottom, more capital is concentrated in high-capital risk markets.

For example, unlike currency markets, U.S. stocks have underlying performance as an endorsement, and performance is the best measure of a stock's value, while currency markets rely more on consensus. Secondly, as the U.S. major capital representative, USDC did reduce its holding, but the amount of reduction was not very large, nor was it the main force to reduce its holding, but even so, USDC's market value dropped by nearly 100 million US dollars at 8:00 this morning.

The biggest reduction was almost 140 million US dollars directly on DAI. At first glance, this figure might be thought that MakerDao has suffered another large-scale serial passive reduction. Judging from the detailed data, the market value drop occurred at about 18:00 last night, that is, before the release of the CPI data, so we can draw the conclusion that it should be artificial active reduction, possibly because we are worried that bad CPI data will affect the position.

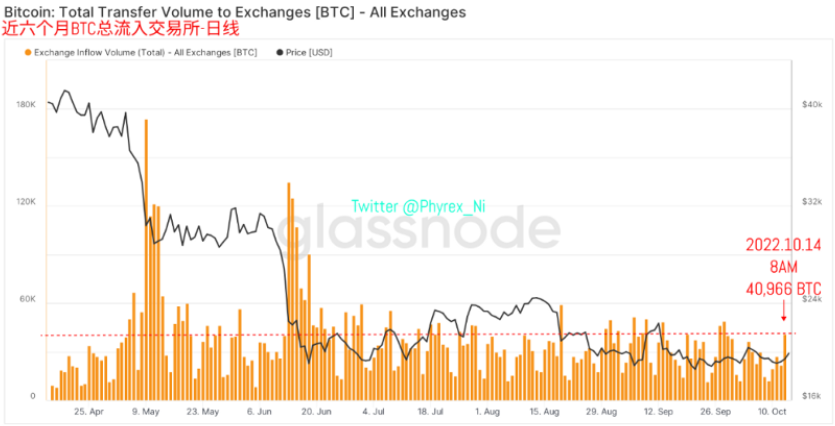

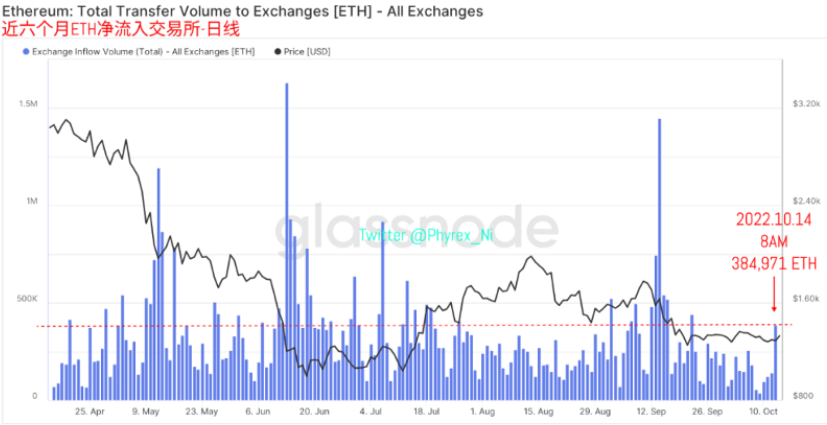

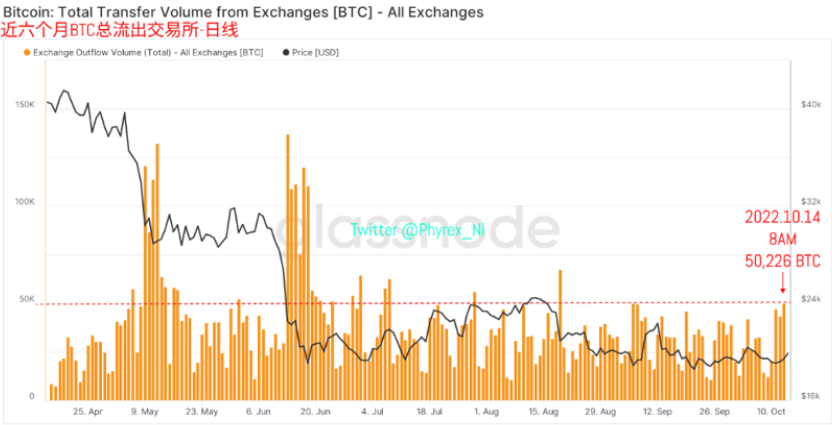

The selling pressure on BTC and ETH was also as large as expected, with large amounts of chips shifting onto the exchanges before the CPI announcement. This, of course, was directly related to the first BTC and ETH price declines at 18 p.m., which turned Binance into the main underwriting exchange for BTC and ETH, and which triggered most of the subsequent declines.

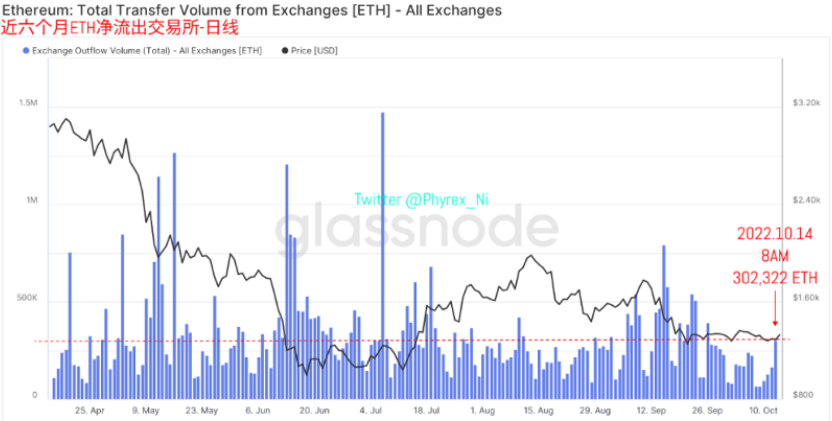

The trend was different from that of selling pressure on BTC and ETH. When the market crashed, BTC did not continue to transfer into selling pressure in large quantities. On the contrary, BTC's lower price led to a larger withdrawal and withdrawal behavior, which directly broke through the minimum inventory of nearly four years. ETH, on the other hand, although there were signs of withdrawal, more than 80,000 chips were transferred into Bitfinex, and they have not left.

So it can't be ruled out that this is the exchange's behavior in sorting out its wallets, especially since there have been a lot of cases like this recently, which is the main reason why there has been a lot of ETH accumulation on the exchange. BTC's stock of exchanges, on the other hand, shrank as its exits rose. It is no wonder that not only yesterday's BTC showed enough resilience to rally, but it is also leading the rally.

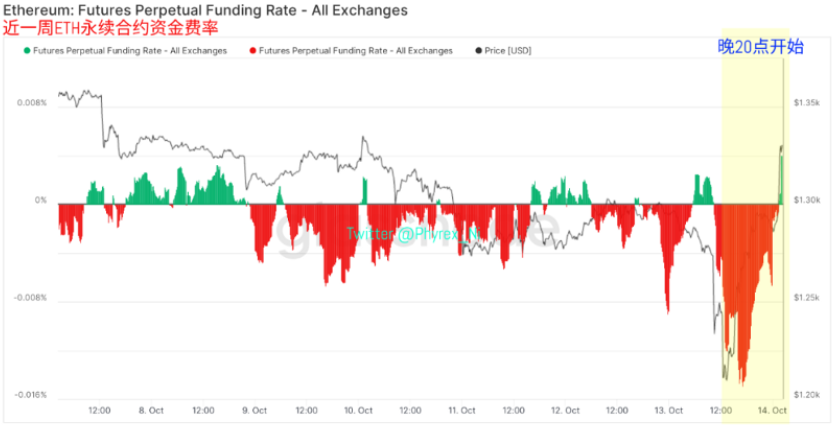

On the emotional side, both the BTC and the ETH are signaling a phased bullish trend, with a slight move in time but mainly a one-sided game, as more investors believe the worst is behind them, with markets already pricing in a 75-basis-point increase in November and a 50-basis-point increase in December.

In summary, although the current BTC and ETH prices have shown a upward trend, it is still difficult to judge whether they have reached the bottom now. A single CPI data can throw off a drop of more than 3%, which also shows that the market sentiment is still tense. The following weekend will be plunged into a situation where the two-way circulation of funds and chips caused by the market makers' vacation is poor, and even more cautious about the possibility of inflation and collapse.