Current Summary:

The minutes of the Federal Reserve's July meeting, released at 2am, yesterday, almost erased the impact of last night's retail sales data. The most immediate reaction was to look at expectations for a September rate hike. The 50 basis point chance of a September rate hike in the run-up to last night's retail sales data was around 61%. Now that there are retail sales data, a 50 basis point hike could be cut to around 48%, less than half. This is a time of panic in the markets. After all, the main game in town for economists is the Fed's easing of interest-rate hikes, which is why even the ultimate goal of lower inflation is this. But if the Fed did not choose to taper its interest-rate hikes in September, the "bottom-fishing" message from economists would have gone awry. It is possible that the bottom in the risk markets has not materialized, and the Fed has not been sending a clear message in recent times. This leads to a gradual depletion of positive information and even fatigue, which is why the Nasdaq's rise is becoming smaller and smaller. But the more fragile positive number is the September rate hike forecast. But last night's retail sales data, which were like a straw in the wind, had a small impact on the macro picture (and were analyzed in detail last night), but they upset the balance and caused a change in macro sentiment. The Fed minutes released at 2 am today were almost interpreted by the market as dovish remarks by the Fed, especially since the July CPI data had not yet appeared. Two important interpretations were positive for the economy, starting with the view of many of the Fed's vote committees that "there is a risk that monetary policy will tighten by more than the necessary amount," which means that the Fed, though in July it decided to raise interest rates by 75 basis points, has already excessively increased rates. Because it was also the first time since the Fed's rate hike that "excessive tightening" might raise risk, there was no mention of the 75 basis-point increase in September in the minutes, so this was interpreted first and foremost as a positive economic interpretation. The second is that the Fed is once again discussing the possibility of a slowdown in interest-rate hikes, which markets interpret as likely to begin in September.

The Fed minutes were the most immediate reaction from markets, with the 50 basis point increase forecast for September having risen from 48% to 63%, erasing the fall from last night's retail sales figures and adding an extra 2%. Therefore, although the Nasdaq still closed lower, looking at the trend of Nasdaq futures after the close, it is still possible that a high opening will be achieved before the opening of trading tonight.

Details of the impact on risk markets were also revealed in the US dollar index, which was almost above 107 after the release of retail sales data last night, but which saw a correction in the DXY following the release of the Fed minutes, which halted the upward trend. But it has to be said that the dollar index is still fluctuating at a high level, which is also very negative for risk markets, and even poses a challenge to whether the DXY index has indeed peaked.

While the dollar index rose yesterday, the yield on short-term Treasury bonds rose above 3.3%, and the yield on medium-term Treasury bonds averaged more than 3%. However, there was no movement of funds into the market until the U.S. stock market closed. Only at 8 a.m. Beijing time did there appear a decline in U.S. Treasury colonial rates, and indeed there was a high purchasing power of U.S. Treasury bonds during the recent Asian morning.

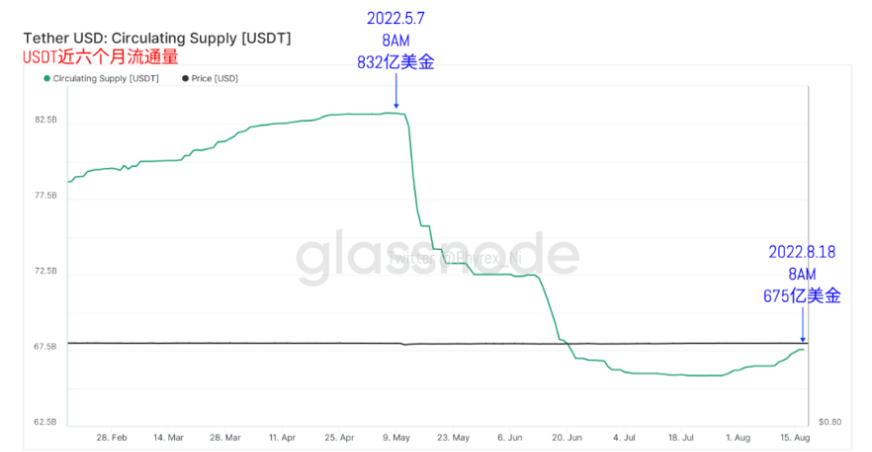

And the impact on the currency market is whether the market value of USDT, which has been increasing in recent years, will continue to rise. And in fact, the concern is true. The market value of USDT has increased, but only by about $1 million, down from the previous increase of more than $100 million per day. And USDC's market value is still shrinking, by $90 million at 8:00 this morning. The overall value of the currency market has fallen. It was also the first time in the last two weeks that this had happened. Of course, the current game is still continuing, and the current macro sentiment is back to a favorable economic sentiment, so it is obvious that not only the downward trend of the BTC and the ETH has been alleviated, but even there are some signs of a slight rebound, which also shows that the confidence of users in the currency market and the purchasing power have increased.

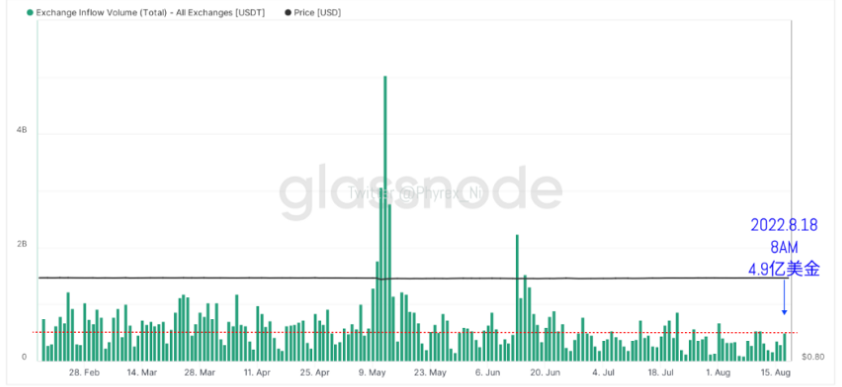

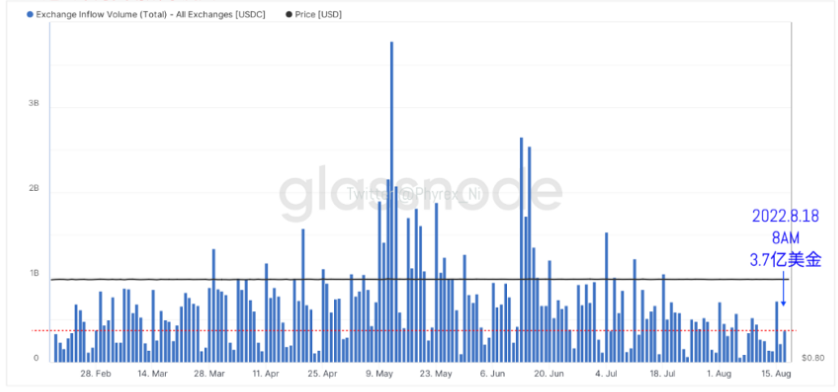

Indeed, up to 8:00 a.m. this morning, capital into the exchange data, both USDT and USDC have improved, although still far from the high, but compared to the low point of the previous period is also good, especially the amount of capital USDT increased significantly, indicating that the market is not without money, but waiting for a more appropriate price, so from last night to early this morning macro sentiment changes promoted the fate of funds. The details of the money show, first, that USDT still shows strong signs of entering Europe's main time zones, and a strong shift in activity was seen between 8 p.m. yesterday and 6 a.m. this morning, especially after retail sales figures and the Federal Reserve minutes showed that the main money is still thinking about buying low, and that lower prices or better trends could trigger entry. Moreover, there was a clear downward trend not only for USDT but also for USDC, especially with the release of the Fed minutes and the stronger inflow of capital since the close of US stocks, which indicated that the macro sentiment has also affected the major US funds, but the more specific situation will depend on whether Europeans continue to increase their purchases this afternoon and what happens after the index opens in the evening. After all, emotions are destroyed, panic is triggered, and it will take time to repair.

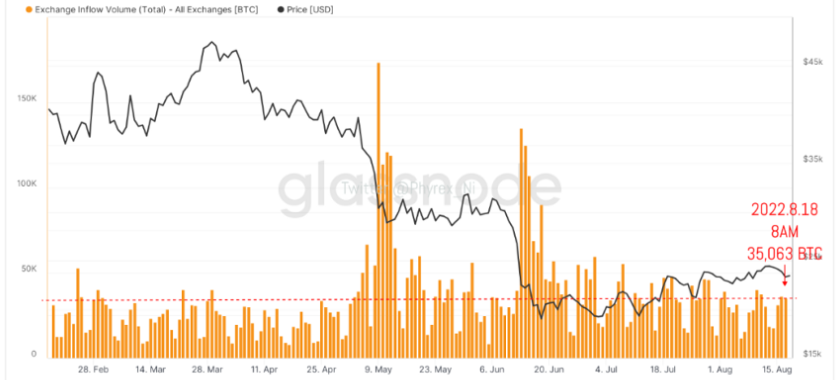

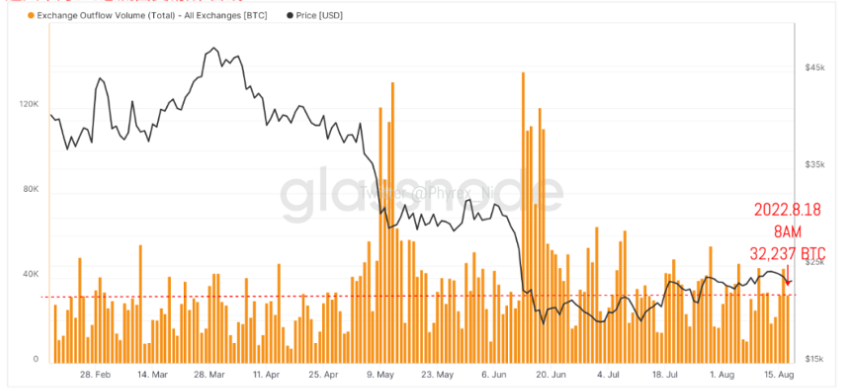

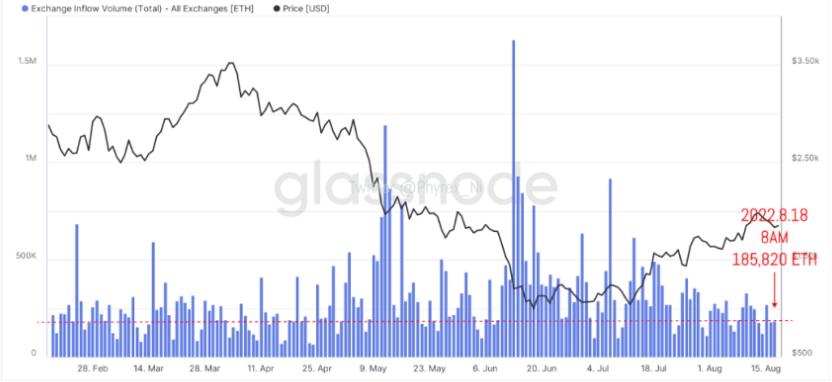

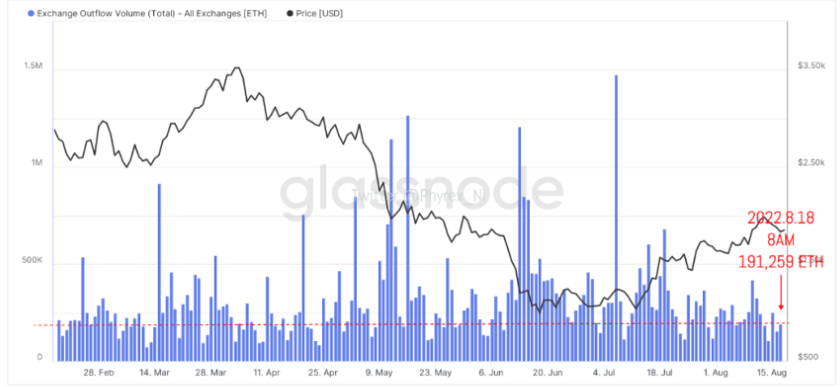

Judging from the selling pressure data from the BTC and ETH till 8:00 a.m., yesterday's selling pressure did indeed increase, which means that although the Fed minutes repaired the users' expectations for the September rate hike, the users' perception of emotions remains extremely sensitive. Especially now, in the absence of obvious favorable circumstances, the long-term shock has already caused the users to be mentally and physically exhausted. Also to 8:00 a.m. this morning the exchange cash transfer data can be seen, falling prices Although the resistance of BTC is more strong, but there are more chips stay on the exchange, ETH is different, embodies the details of the mood changes, when the mood switch is still increased purchasing power, of course, this is also because of the merger of ETH good effect. In particular, the detail data shows that Asian capital has sold off BTC and ETH chips while buying US Treasuries, but there is no obvious corresponding in the ETF data at the same time. This shows that the current buying power cannot cover the selling pressure at this time. So today's trend will remain volatile. The price recovery will depend on the attitude of European and US capital.