Yesterday's video was deeply felt because it was the role of macro sentiment, judging risk markets rather than relying on mysterious indicators. Understand the structure of the risk market, understand the basis of judgment, although can not be accurate to the specific price, but still can grasp the trend of the trend. It is also stressed again in the video that the dollar index is now pre-positioned for Nasdaq futures, while gold is pre-positioned for BTC and ETH. And the reason they cite in this context is not to reiterate how accurate judgments are, but to make more of them actually realize how important macro-emotional judgments are in today's risk markets, and that much risk can be avoided by finding the sharpest possible comparator. The big game remains the Fed's rate hike in the coming December, and the more money-sensitive dollar index is the best guide.

After all, NASDAQ futures are influenced by many factors, including market expectations, and hedging of funds and especially of foreign exchange is not only for small and medium-sized retail investors, but also for top-tier institutions, and even for sovereign sovereigns. The funds available to a country and the assessment of risk, especially at this moment in time, are most pronounced against the US dollar.

While the market is emotionally beginning to accept the Fed's expectation of a 75-basis-point increase in November, that does not mean that a 75-basis-point increase will have no effect on markets. More importantly, it has become clear that the current battle of the dice is stretching into December, when the Fed not only raises rates last in 2022, but also bears the burden of whether the Fed will "shift" toward a 50-basis-point increase, which means that the overall rate hike is already at an end. At least risk markets have already been bottoming out at some stage, especially as a result of the US mid-term elections. Democratic parties are bound to create a buoyant situation, which is unlikely to be much trouble for a month or two. With the Fed's "first mover, second mover", it is bound to have some impact on inflation. At the very least, it is bound to control employment by depressing economic growth and so lowering inflation by pushing down costs.

But if December's rate hike is not 50 but 75 or higher, there is no way to tell whether 5% will be the final rate for the Fed's hike. If not, how much higher the final rate will be? In fact, the market is ambivalent about CPI, hoping to reduce the Fed's share of rate hikes based on inflation data when CPI is falling, and unwilling to raise rates further when inflation is rising because of rising prices.

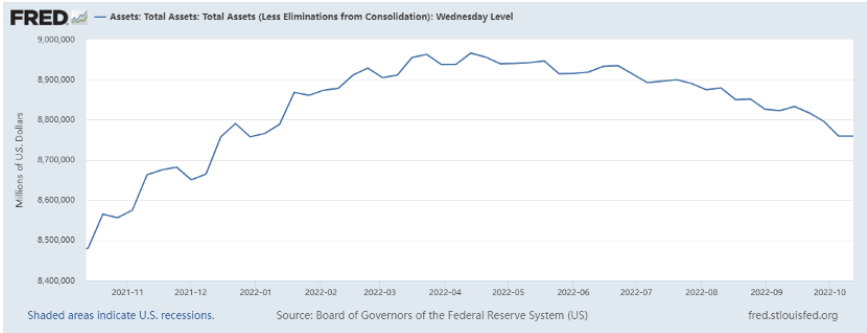

But the Fed has only two options for fighting inflation: raising interest rates and shrinking the balance sheet, which will bring down the economy and employment, and shrinking the balance sheet, which will bring down US debt and savings. neither of them is an unlimited weapon, so many of our little friends ask again why the Federal Reserve can't just raise interest rates forcefully at the start to reach a neutral rate quickly enough to bring down inflation. It's not that the Fed doesn't want to, but rather that it wants to accommodate a direct recession from a more aggressive soft landing than it might dare.

Indeed, there is no clear evidence that inflation has peaked, and even now it cannot be ruled out. Not only are transportation costs rising, food prices staying high, and the cost of housing and rent still trending slightly higher; even today's one-year inflation expectations at the University of Michigan, at 5.1%, are significantly above expectations. And how risk markets bottomed out, with inflation peaking.

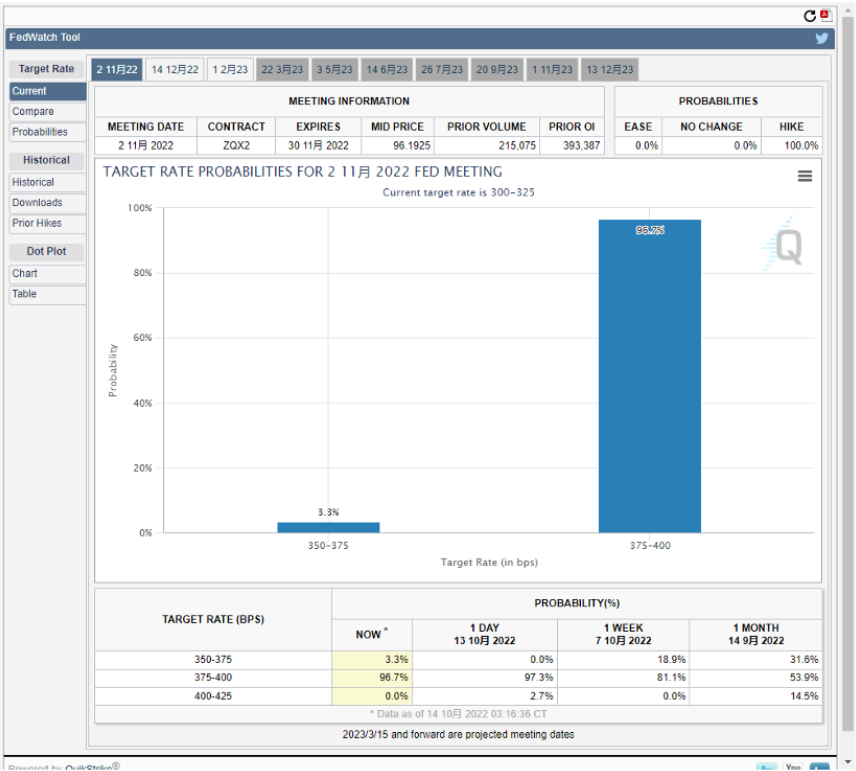

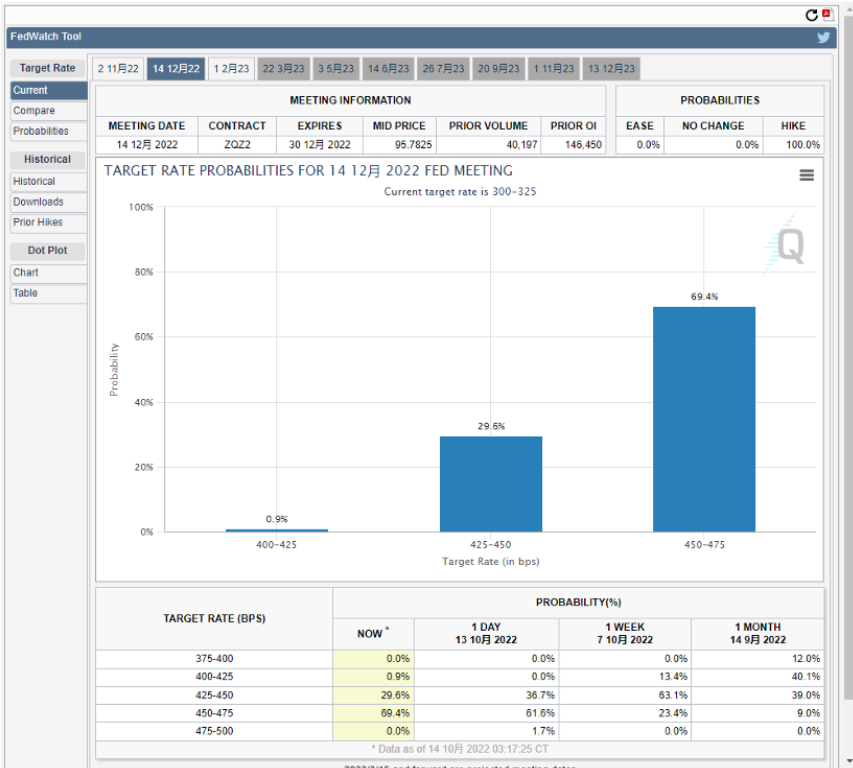

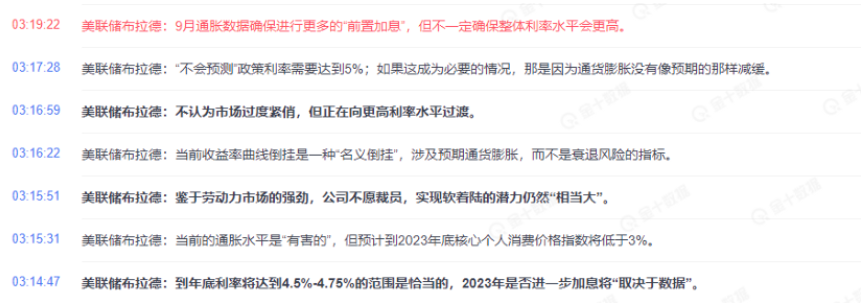

As of 4 a.m. Beijing time, the Nasdaq futures closed higher after falling 3%, while the dollar index rose 0.7% to 113.2, meaning that the Fed's next move to raise interest rates remains highly controversial in today's investor sentiment. But the comments by Fed hawk Brad Pitt, coming before the close of trading today, added to the sense of a two-point game. The first is year-end federal funds rate expectations. At present, 4.5-4.75% implies a 75+50 increase in November and a 75+75 increase in December. This confirms what has been said before. If the latter is followed, there is a high probability that the current risk market will not be at the bottom. The bottom cannot be determined until inflation is announced in October, and it cannot even be ruled out for the year. The second is whether the overall end rate will be 5% or higher, and from Brad's remarks, it is clear that the trigger for a 5% tipping point is likely to be inflation in October, with December's hike peaking at 4.75% year-end, which means the October and November CPI readings are not ideal, forcing the Fed to use a fifth 75 basis point increase, which implies a further hike in 2023. The first increase in 2023 was in February, so a month's inflation would have made it clear, but with a 75 basis point increase in December, the greater probability is that there will be at least one increase in 2023, bringing the overall federal funds rate to at least 5%. The basis for judging the end of 2023 is whether it will continue to move upwards, and if it does, the 56-year run of post-election US share gains will be over.

The good news, though, is that with US stocks closed for the day and downside guidance ends, it remains to be seen whether the risk market will digest expectations and stop the rout in two days' time over the weekend. But with market makers now on holiday, the money market will run out of liquidity, and both the BTC and the ETH could experience a wild rally or bust - after all, as a weekly reminder that a small amount of money can be thrown and a small amount of money can be pulled.

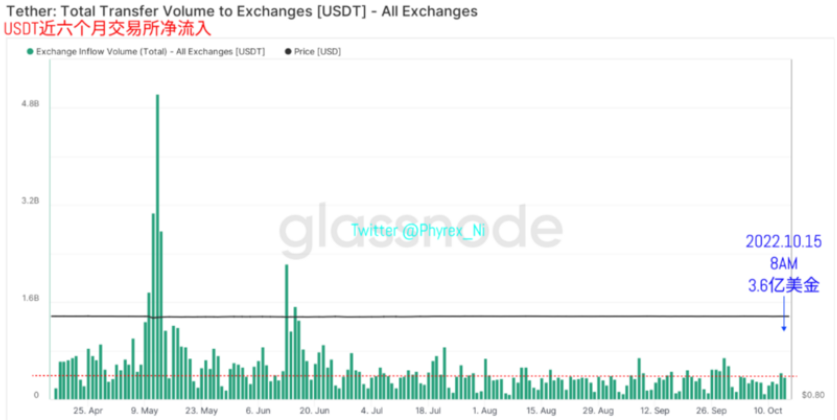

Looking at the market value of the Stablecoin, USDT, which was the main trading force, saw a small increase in market value, around $6 million. Not a lot, but the increase in market value is a good thing, because it represents more European or Asian investors who are bullish on the next leg of the currency market, and BUSD, which was the secondary trading force, still has no change in market value. The slight changes in the USDT and BUSD overall also suggest that the market is currently cold.

On the other hand, the market value of USDC, which represents the major funding source in the United States, has again dropped, and is still dropping, by 8:00 this morning, directly more than $550 million, the largest single-day drop in recent months. As the dollar index continues to rise, it is hard to see a price rebound in the currency market, and American confidence is gradually being destroyed.

And there is only one final step before USDC's market value falls below $45 billion. DAI's market value has continued to decline, down only $70 million, but the decline as a percentage of the lower-cap DAI is still large, and represents investor discomfort with ETH's continued decline. The market value of the four main stablecoins closed around $640 million lower as the weekend began.

Although the market value of USDT has increased a little, but from the purchasing power point of view, it still shows the overall downward trend. In the recent two consecutive days, both BTC and ETH have shown large fluctuations. Comparing the financial strength of USDT, which is the main trading force, with that of the first half of the year, we can see a clear gap. Even if CPI can trigger changes in macro sentiment and fluctuations in the currency market price, the amount of capital that can be converted into purchasing power is also decreasing.

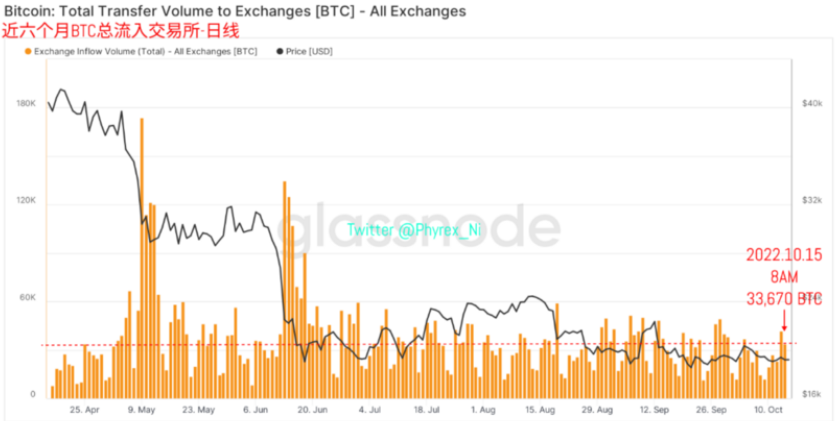

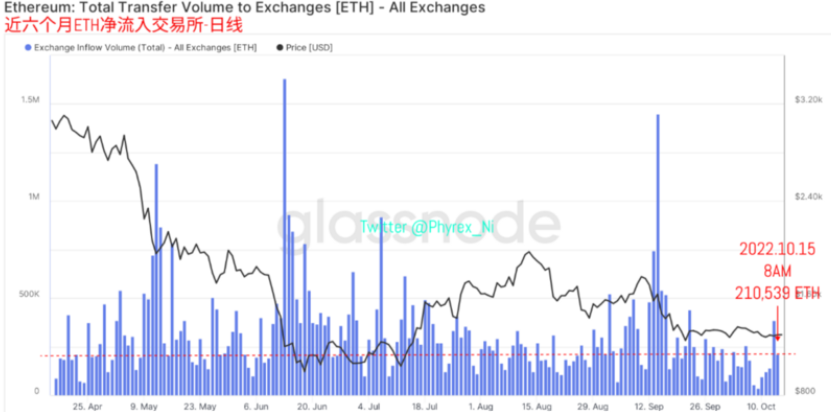

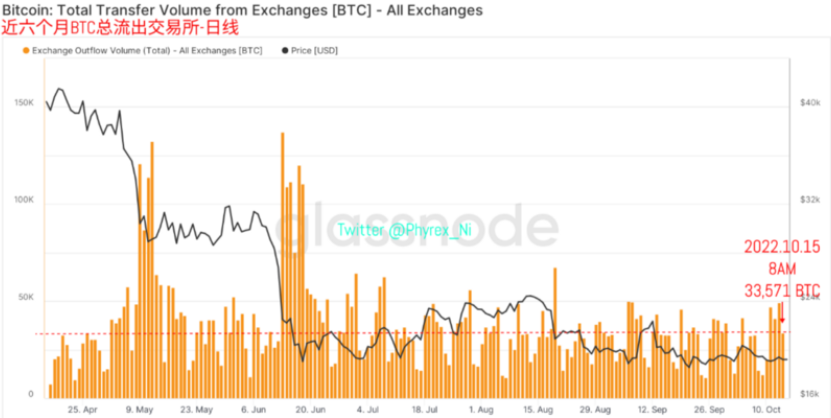

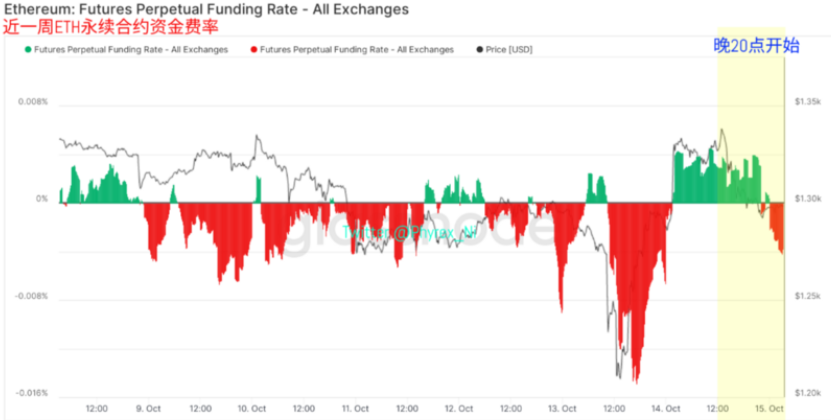

Although the BTC and ETH prices also continue to decline with the index futures, but compared to the release of CPI before and after two large declines, both BTC and ETH have shown strong resilience, the main reason is that selling pressure has decreased significantly, especially ETH selling pressure, compared to the previous day reduced about 30%, and selling pressure reduction is the main reason for price stability.

Relatively reduced selling pressure, from the exchange of cash withdrawals also appeared a larger decline, which can be guessed from the purchasing power reduction, and the BTC withdrawals can not even cover the overall selling pressure, so more chips remain in the exchange, although the ETH withdrawals data will be stronger, perfect coverage of selling pressure, but the extent of selling down for high stock consumption is only a drop.

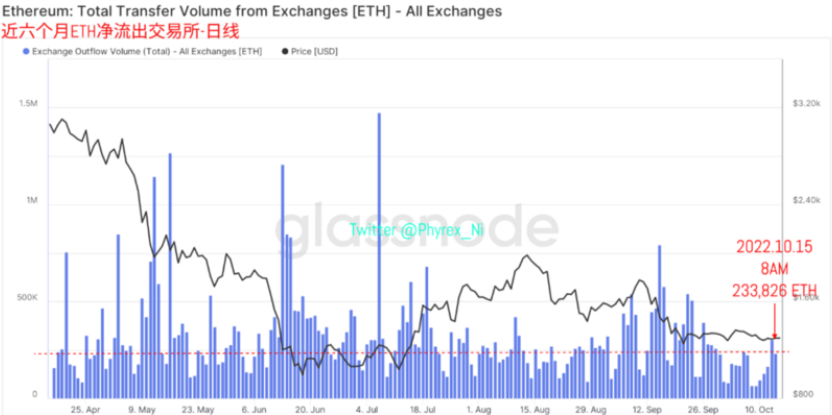

It is also obvious from the stock exchange's inventory that the inventory which broke the BTC's minimum inventory for nearly four years yesterday rose by a small amount due to the decrease of purchasing power. However, ETH, as mentioned earlier, said that although the inventory has decreased, the magnitude of the decrease is still too low. It will still face heavy selling pressure on the inventory which is still at a high level.

And from the long-term holding of BTC trend is also not difficult to find, although the macro sentiment appears to be more obvious changes, leading to the decline in the currency market, but the long-term holding of chips has not been reduced, much less generate panic, but is consistent with the past and continue to increase the holding, which represents the falling price, the high lock-up chip has been in a downward trend mentally and physically, almost to ignore the price trend.

Finally, from an emotional perspective, although the Nasdaq futures drove down the BTC and ETH before the close, there was no guidance for the Nasdaq futures after the close and no market makers. Instead, both the BTC and the ETH experienced post-stop small swings. The emotional side of the BTC was slightly more bullish, while the bearish side of the ETH was more pronounced, which is normal for weekends when the trend continues to be volatile. In summary, at the end of a week, prices in China's currency market will be relatively stable. Take advantage of rare opportunities and rest with your family for a while. Enjoy two days of peace and quiet. As third-quarter earnings season progresses next week, two days of sideways changes are likely to occur. Particularly if the macro sentiment side is shaky, something may trigger an already fragile nerve.