Wondering "do I need a license for a crypto startup?" In 2026, the answer is yes. Learn how to avoid frozen bank accounts and fast-track your compliance with a Canadian MSB.

Elena Vance was staring at her laptop in disbelief. As the founder of a rising Web3 payment protocol, she had just secured a major partnership to help DAOs pay their global contributors in fiat. Everything was moving flawlessly...ehmmm, well, until a Friday morning email from her Tier-1 correspondent bank changed everything.

$1.2 million in operational funds had been frozen without warning. The reason? A sudden "internal risk reclassification." Because her operating entity was processing fiat-to-crypto transactions without a formal regulatory status, the bank flagged her protocol as an unregulated high-risk shadow processor. Her contributors were going unpaid, the project's reputation was crumbling on social media, and traditional lawyers were quoting her 12 months and $50,000 just to start a compliance application in Europe.

Elena’s nightmare is no longer an isolated incident; it is the new reality of "de-risking" in the Web3 industry.

When founders see this happening to their peers, the immediate question that echoes in every boardroom is:

Do I need a license for a crypto startup in 2026?

The short answer is an absolute yes. The "Wild West" era of blockchain business is officially over. Today, operating without a regulatory framework doesn't just invite government fines, it guarantees that the traditional financial system will lock you out entirely.

But there is a silver lining. While the traditional path to compliance is a bureaucratic trap that can drain your runway, there is a legal fast-track that your competitors don't want you to know about.

In this comprehensive guide, we will break down the exact legal risks of remaining unlicensed, why Tier-1 banks are ghosting offshore companies, and the ultimate fast-track shortcut to secure a fully approved regulatory setup for your crypto business.

The "Friday Morning Nightmare": This is the reality for founders operating unlicensed crypto startups when Tier-1 banks de-risk their accounts. Don't wait until your funds are locked to ask about compliance.

Why You Need a Crypto Startup License: The Banking Reality

When Elena demanded an explanation from her legal team about the frozen $1.2 million, they didn't point to a courtroom, they pointed to the bank's strict compliance algorithms. For founders currently asking, "do I need a license for a crypto startup in 2026?", the answer is a resounding yes. However, the primary reason to get licensed today is no longer just the fear of government prosecution; it is the immediate financial paralysis of your business operations.

Unlicensed crypto exchange penalties and legal risks in 2026

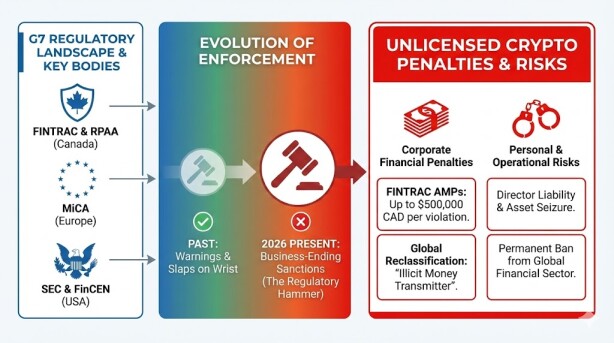

Let’s look at the regulatory hammer first. In previous bull runs, financial authorities issued warnings. Today, they issue business-ending sanctions.

The unlicensed crypto exchange penalties in 2026 have escalated dramatically across all G7 jurisdictions. Under Canada's FINTRAC framework and the fully enforced Retail Payment Activities Act (RPAA), operating a fiat-to-crypto gateway or acting as a Money Services Business (MSB) without proper federal registration is treated as a severe financial offense.

Regulators are no longer lenient. Failure to register can result in Administrative Monetary Penalties (AMPs) reaching up to $500,000 CAD per violation. Furthermore, in Europe under the MiCA framework, or in the US under the SEC and FinCEN, unregistered operators are immediately classified as illicit money transmitters. You are not just risking a corporate fine; directors are risking personal liability, asset seizure, and a permanent ban from the global financial sector.

The Regulatory Hammer: A visual breakdown of how global enforcement against unlicensed crypto startups has escalated to business-ending sanctions in 2026.

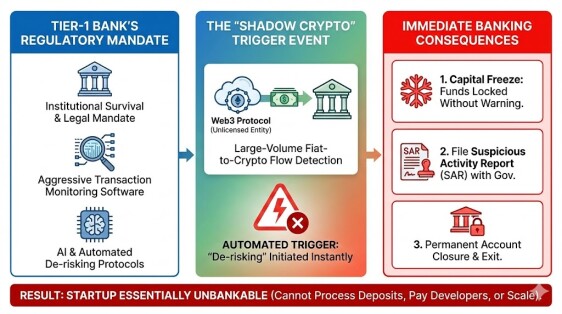

Why Tier-1 banks freeze "shadow crypto" accounts

Even if you mistakenly believe your startup can fly under the regulatory radar, the banking sector acts as the ultimate, unforgiving gatekeeper. This was exactly Elena’s downfall. Her protocol was moving millions in fiat into Web3, acting as a "shadow" processor without the legal wrapper of a recognized compliance license.

The reason why Tier-1 banks freeze "shadow crypto" accounts comes down to their own institutional survival. Financial institutions are mandated by law to use aggressive transaction monitoring software. The moment their AI algorithms detect large-volume crypto-related fiat flows from an unlicensed corporate entity, automated "de-risking" protocols are triggered instantly.

The bank will not call you to ask for an explanation. They will freeze the capital, file a Suspicious Activity Report (SAR) with the government, and permanently close your account. Without a recognized regulatory passport, such as an active Canadian MSB or FMSB license—your startup is essentially unbankable. You cannot process user deposits, you cannot pay your developers, and you cannot scale.

The Banking Death Spiral: See how automated bank AI triggers instant capital freezes for startups trying to operate without a license.

Do DeFi Projects & DAOs Really Need an MSB License in 2026?

One of the most dangerous myths in the Web3 space is the "Decentralization Illusion." Many founders believe that because their project is governed by smart contracts and runs on a blockchain, they are somehow exempt from traditional financial regulations. They assume that "code is law" and that having no central CEO means there is no one for regulators to penalize.

In 2026, this assumption is a fast track to getting shut down.

When technical founders ask, "do DeFi protocols need a license?", the answer depends entirely on the flow of funds and the user interface. Regulators like FINTRAC, the SEC, and European authorities (MICA) do not care about your tech stack. They care about the financial activity. If your protocol facilitates the exchange of digital assets, provides yield-generating liquidity pools, or most importantly, connects to a fiat on-ramp (allowing users to buy tokens with credit cards), you are conducting regulated financial activities. The fact that it happens on a blockchain does not erase your Anti-Money Laundering (AML) obligations.

But what if you are structured as a Decentralized Autonomous Organization (DAO)?

Regulators have adapted. Claiming "we are just a DAO" is no longer a valid legal defense. Authorities now look for the "controlling minds" behind the project: the developers holding the multi-sig wallet keys, the founders who launched the token, or the company hosting the front-end website. If you provide the interface that connects retail users to decentralized finance, you are viewed as a financial intermediary.

Furthermore, even the most decentralized projects cannot escape the real world. You still need to pay your core developers, cover server costs, hire auditing firms, and fund marketing campaigns. To do this, your DAO needs to convert crypto into fiat currency. But a traditional Tier-1 bank will never open a corporate account for a "smart contract."

This is where the reality of DAO crypto compliance hits hard. To interact with the real world, your decentralized project must establish a centralized "Operating Entity" (often called a DevCo or Foundation). And if you are still wondering, do I need a license for a crypto startup in 2026?, the answer is that this Operating Entity absolutely does.

The Compliance Bridge: Regulators and banks require DAOs to establish a licensed "Operating Entity" to handle fiat transactions and real-world expenses legally.

Without a recognized compliance wrapper—like a Canadian MSB license—your DAO's operating entity will never secure the banking relationships needed to bridge your on-chain treasury with off-chain expenses. You need a licensed corporate bridge, and you need it before the regulators knock on your door.

What Happens if I Launch a Crypto Token Without a License?

The days of anonymous founders raising millions through a simple website and a whitepaper are dead. Yet, many developers still ask, what happens if I launch a crypto token without a license?

The assumption is that as long as it is a "utility token," regulators will look the other way.

This is a dangerous miscalculation. When you mint and distribute a token (whether through an ICO, IDO, or even a targeted airdrop) without a regulated corporate entity backing it, you face two massive roadblocks that will instantly kill your project's momentum.

1. The Regulatory Hammer (The Securities Trap)

First, regulators do not care what you call your token; they care about how it functions. In the US, the SEC applies the Howey Test, and similar frameworks exist under Europe's MiCA and Canada's securities laws. If you are selling a token to fund your project's development, and buyers expect a profit based on your team's efforts, you are likely issuing an unregistered security.

The penalty?

Regulators will force you to halt operations, refund investors, and pay crippling fines.

The Tier-1 Exchange Bottleneck (The Binance Reality)

Even if you manage to avoid a government subpoena, you will hit a brick wall when trying to build liquidity. Let’s talk about the ultimate goal for most Web3 startups: getting listed on Tier-1 exchanges like Binance, Coinbase, or Kraken.

Historically, exchanges were lenient. But in 2026, after historic DOJ settlements against giants like Binance and massive regulatory crackdowns, Tier-1 exchanges have completely overhauled their listing requirements.

If you approach Binance's listing committee with an unregulated token launched by an anonymous DAO or a shell company, your application will be instantly rejected. Today, top-tier exchanges require comprehensive due diligence. They demand to see your corporate structure, your legal opinions (proving the token is not a security), and your active compliance framework (like an MSB registration) to ensure you are meeting Anti-Money Laundering (AML) standards.

Simply put: Launching a token without a license means no market makers will touch you, Tier-1 exchanges will ignore you, and your token will be permanently trapped in low-volume, decentralized liquidity pools.

To give your token real value and global access, you need a legitimate "token issuance entity"—a fully compliant corporate bridge that proves to the market and exchanges that you are a serious, regulated player.

The Two Roadblocks: A visual breakdown of why launching an ICO or token without a compliant corporate entity guarantees regulatory fines and instant rejection from Tier-1 liquidity markets.

The 2026 Regulatory Landscape: Offshore vs. Onshore

Once a founder accepts that the answer to "do I need a license for a crypto startup in 2026?" is a definitive yes, they immediately make their second biggest mistake: they look for the cheapest and fastest option on the internet.

In the early days of Web3, setting up a shell company on a tropical island was the standard playbook. Today, choosing the wrong jurisdiction will drain your capital just as fast as having no license at all.

Let’s break down the reality of the global map.

Why offshore crypto licenses (Curacao, Panama) are dying

A few years ago, aggressive marketing agencies sold thousands of offshore crypto licenses in jurisdictions like Curacao, Panama, or Vanuatu. The pitch was tempting: pay a few thousand dollars, get a license in three weeks, and avoid strict audits.

But here is the harsh reality in 2026: an offshore license is just an expensive piece of paper if it doesn't give you access to a bank.

Tier-1 financial institutions have completely blacklisted or heavily restricted these regions. If you walk into a reputable European or North American bank with a Panamanian crypto license, the compliance officer will reject you before you even sit down.

Here is exactly why the offshore route is effectively dead for serious startups:

-

The Banking Black Hole: Traditional banks view offshore crypto entities as extreme money-laundering risks. You will be forced to use shady, high-fee payment processors that can freeze your funds at any moment.

-

Investor Repellent: Venture Capital (VC) firms in 2026 are heavily audited. They are legally restricted from injecting millions of dollars into unregulated offshore entities. If you want institutional funding, an island license is a massive red flag.

-

G7 Regulatory Pressure: Global watchdogs are actively squeezing offshore tax havens. What is legal in Vanuatu today might be globally sanctioned tomorrow.

The MiCA (Europe) vs. FINTRAC (Canada) Standard

To survive and scale, you must move "Onshore" to a respected, G7-level jurisdiction. The crypto compliance requirements 2026 demand a corporate structure in a country that banks actually trust. Right now, there are two gold standards dominating the global market: Europe and Canada.

The European Route (MiCA): The Heavyweight Option

The Markets in Crypto-Assets (MiCA) regulation has made Europe a safe haven for legal clarity. However, it is built for corporate giants, not agile startups. Applying for a MiCA-compliant license from scratch means hiring local directors, locking up massive amounts of operational capital, and waiting anywhere from 12 to 18 months for approval. It is a fantastic framework, but it is too slow and expensive for a project that needs to launch next month.

The Canadian Route (FINTRAC): The Agile Gold Standard

This is where Canada has emerged as the ultimate strategic winner for Web3 founders. Operating as a registered Money Services Business (MSB) under Canada's FINTRAC gives you the perfect balance.

-

It is a G7 nation, meaning Tier-1 banks worldwide respect the license and will eagerly open corporate accounts for you.

-

It proves to users and investors that you meet top-tier Anti-Money Laundering (AML) standards.

-

The regulatory framework is clear, business-friendly, and designed to foster fintech innovation without suffocating it with European-style bureaucracy.

If you want the prestige and banking access of a top-tier nation without the year-long waitlist of Europe, the Canadian FINTRAC standard is exactly where your startup needs to be.

The 2026 Reality Check: Why saving a few thousand dollars on an offshore license will cost you your banking access and investor confidence.

💡 Founder's Shortcut: Are you already realizing that your DAO or Web3 startup needs a G7 compliance wrapper today? Don't wait until your runway dries up.

We hold an exclusive inventory of fully licensed, Ready-Made Canadian MSBs ready for an immediate transfer. Send me a quick message on Telegram to see what we have available right now, or keep reading to see exactly why applying from scratch is a 12-month trap.

The 2 Paths to Legalize Your Crypto Startup

So, you’ve survived the reality check. You know that launching without a compliance wrapper is institutional suicide, and you know that offshore islands are blacklisted by the global banking system. The question is no longer "do I need a license for a crypto startup in 2026?", the question is how the hell do you get one before your runway dries up?

When it comes to acquiring a G7-level license like the Canadian FINTRAC MSB, you have two choices. One is a bureaucratic nightmare; the other is the industry's best-kept secret.

Path 1: Applying from scratch (The 12-Month Trap)

Let’s start with the traditional route. You hire a legacy law firm that probably still thinks Bitcoin is "magic internet money." They will gladly charge you $800 an hour just to "research" the crypto compliance requirements 2026.

Here is what applying from scratch actually looks like in the real world:

-

The Paperwork Avalanche: You must incorporate a new entity from zero, draft hundreds of pages of custom AML manuals, and build a compliance program.

-

The Waiting Game: You submit your application to regulators and wait in a massive backlog with thousands of other desperate founders.

-

The Cash Burn: This is the deadliest part. While you wait 9 to 14 months for the government to approve your license, you are still paying your developers, your server costs, and your marketing team.

By the time you finally get your approval a year later, the bull market might be over, or a competitor with less friction has already stolen your market share. Doing it from scratch is financially exhausting and strategically slow.

Path 2: Buying a Ready-Made Canadian MSB (The Turnkey Solution)

Now, let's talk about the cheat code. What if you didn't have to wait in line? What if you could skip the regulatory queue entirely and just buy a company that has already survived the gauntlet?

Enter the "Ready-Made" or "Shelf" Company.

A Ready-Made Canadian MSB is a corporate entity that was incorporated months ago, went through the brutal FINTRAC application process, and successfully secured its active Money Services Business license. However, it has zero financial history—no operations, no clients, no baggage. It is essentially a clean, fully licensed shell waiting on a shelf for an owner.

Instead of applying from scratch—which currently takes 2 to 4 months even in a fast-moving jurisdiction like Canada—you simply acquire an existing, already-approved company. The corporate transfer of ownership and directorship is expedited and completed in a matter of weeks. Let that sink in.

In a fraction of the traditional timeframe, you go from being an unbankable "shadow crypto" project to the legal owner of a premium, G7-regulated financial entity.

-

Instant Banking Access: Because the entity is already licensed, you can immediately initiate onboarding with crypto-friendly Tier-1 banks and fiat payment processors.

-

Launch Speed: Your protocol can go live, connect to fiat on-ramps, and onboard retail users legally in a matter of weeks, not years.

-

Cost Certainty: Instead of a black hole of hourly legal fees that change every month, you pay a flat, predictable acquisition cost.

Remember Elena from our introduction? If she had spent a fraction of her frozen capital on acquiring a Ready-Made Canadian MSB, she wouldn't be fighting government subpoenas today. She would be scaling her user base.

Ultimately, compliance in 2026 is no longer just a legal shield to keep you out of jail. It is your strongest marketing asset. A G7 license proves to users, Tier-1 exchanges, and VC funds that your startup is built to last, while your unregulated competitors get shut down.

Conclusion: Secure Your Crypto Compliance Today

Let’s wrap this up. If you started reading this article wondering "do I need a license for a crypto startup in 2026?", you now have your definitive answer. The "wild west" era of Web3 is officially over. Operating without a solid corporate and legal framework is no longer a rebellious growth hack; it is simply a countdown to disaster.

Do not wait until a compliance officer freezes your corporate funds, or until Tier-1 exchanges laugh you out of their listing committee. Meeting the strict crypto compliance requirements 2026 does not have to mean burning a year of your startup's runway on clueless legacy lawyers.

You have the opportunity to take the fast-track shortcut.. By acquiring a Ready-Made Canadian MSB, you bypass the bureaucratic red tape, secure top-tier G7 banking access, and get back to doing what you actually do best: building your product and scaling your community.

We have a curated, exclusive inventory of fully licensed, clean Canadian MSB shelf companies ready for immediate transfer. Stop gambling with your project's future.

Send us a direct message on Telegram to see our current list of available Canadian MSBs.

Let’s get your startup compliant, globally bankable, and live without the 12-month wait

The Founder's Reality: Stop stressing over frozen accounts and regulatory threats. Secure your Ready-Made Canadian MSB today, answer the "do I need a license for a crypto startup in 2026" question once and for all, and unlock global liquidity for your project.

FAQ: The Founder’s Reality Check

1. Okay, I get it, but honestly... do I really need a license for a crypto startup in 2026 if I'm just a small team testing a beta product?

Yes. Traditional banks and regulators do not care about the size of your team; they care about the flow of fiat money. Even in a beta phase, if your product touches fiat currency or acts as a bridge for digital assets, automated banking algorithms will flag you. Securing a license early prevents you from getting permanently blacklisted by payment processors before your official launch.

2. I'm planning to drop a utility token next month. What happens if I launch a crypto token without a license right now? Am I going to jail?

You likely will not go to jail on day one, but your project will be "dead on arrival." Unlicensed tokens face instant rejection from Tier-1 exchanges, and legitimate market makers will refuse to provide liquidity. Without a corporate compliance wrapper backing the token, it will be trapped in low-volume decentralized exchanges, and your investors will quickly lose faith.

3. We are a DAO with no central CEO. How does DAO crypto compliance even work? Who actually holds the license?

This is a very common challenge. Regulators focus on the "operating entity" (the team building the front-end or managing the treasury). To comply, DAOs set up a legal corporate wrapper—like a Canadian MSB—to act as a bridge to the real world. This compliant entity holds the bank account, pays the developers, and holds the license, while the DAO community continues to govern the protocol's smart contracts.

4. Buying a "Ready-Made Canadian MSB" sounds a bit too good to be true. Am I buying someone else's hidden debts or legal problems?

That is a very valid and smart concern. However, these are strictly "shelf companies." This means they were legally incorporated and put through the strict FINTRAC licensing process for the sole purpose of being sold to founders like you. They have absolutely zero financial history, zero past clients, and zero operations. You are acquiring a 100% clean slate with a pre-approved regulatory status.

5. A guy on Twitter said he got a crypto license in Panama for $3,000. Why shouldn't I just do that instead of Canada?

Because that $3,000 offshore license will not get you a bank account. The strict crypto compliance requirements 2026 are entirely focused on banking access and institutional trust. Tier-1 banks in Europe and the US have blacklisted jurisdictions like Panama and Curacao. Canada gives you G7 prestige, meaning global banks will actually open their doors for you.

6. Let's say I take the risk and operate in the shadows for a few months. What are the actual unlicensed crypto exchange penalties in 2026?

The era of receiving a polite "warning letter" is over. Today, the penalties mean severe financial ruin. In Canada, operating an MSB without registration can result in fines up to $500,000 per violation. In the US and Europe, it results in the immediate freezing of all corporate funds and potential personal liability for the founders. It is simply not worth the gamble.

7. You mentioned an expedited transfer for the Ready-Made MSB. Is that a marketing gimmick? Can I actually open a bank account immediately?

The fast-track timeframe is real and covers the legal transfer of the corporate entity and the active FINTRAC license into your name. Once that transfer is complete, you instantly become a regulated entity and can begin the onboarding process with crypto-friendly banks. While the bank's internal compliance checks take their own time, you completely skip the 9 to 12 months it would have taken to get the MSB license approved from scratch.

8. Okay, say I buy the Canadian MSB. Do I need to hire an army of expensive compliance officers to keep it active?

Not at all. The Canadian framework is highly respected but designed to be agile and business-friendly. You will need a designated compliance officer (which can be a trained member of your own team) and a solid AML manual (which is typically included in your setup). It requires straightforward, manageable reporting—not the crushing bureaucracy of European frameworks.

9. If I get a Canadian MSB, does that mean I can only have users from Canada? My market is global.

Your market remains completely global. The Canadian MSB acts as your globally recognized corporate headquarters. Because it is a highly respected G7-regulated entity, it gives international partners, payment processors, and global retail users the trust they need to do business with you, regardless of where they live.

10. I'm scared my bank is going to freeze my funds soon. If I message you on Telegram, what exactly happens next? Am I committing to buy immediately?

Absolutely not. When you send a message, we will just have a casual, strictly confidential chat about your specific project and your current bottlenecks. I will show you the current inventory of Ready-Made MSBs, explain the exact transparent costs, and answer any technical questions. You only move forward when you feel 100% confident that this is the right strategic move for your startup.

11. I just want to build a cool Web3 app, not a bank. At what point do regulators actually classify my project as a "crypto fintech" that needs an MSB license?

The line is crossed the exact second you touch fiat currency or act as a financial intermediary for your users. You might view your project as a humble Web3 startup, but if your platform allows users to buy tokens with a credit card, holds custody of their funds, or bridges fiat to digital assets, global regulators officially view you as a crypto fintech.

That classification automatically triggers strict Anti-Money Laundering (AML) laws, making a compliance wrapper like the Canadian MSB mandatory to keep your operations legal.

12. What if my crypto startup only processes crypto-to-crypto transactions? No fiat, no credit cards. Do I still need to worry about all these 2026 compliance rules?

This is a shrinking gray area. While purely decentralized, non-custodial crypto-to-crypto protocols face less immediate friction from traditional banks (since there is no fiat involved), you still have to survive in the real world. You need to pay your developers, cover server hosting, and fund marketing campaigns. To cash out your corporate treasury, you eventually need a Tier-1 bank account. At the same time, it´s crucial to balance this practical step with a commitment to decentralization, so that, while we integrate these compliance measures, we still uphold the core ethos of our platform.

Furthermore, authorities are actively updating their frameworks in 2026 to bring custodial crypto-to-crypto platforms under the same regulatory umbrella. Securing a Canadian MSB now future-proofs your crypto fintech before the regulatory net closes completely.