The first part of the article:

https://www.publish0x.com/bringing-us-treasurys-onto-the-chain/impermanent-loss-xpzgmkp

How to hedge IL

Though IL seems inevitable, there are some strategies to reduce its negative effect on the profitability of providing liquidity. Let’s look at some of them.

· Stablecoin pairing. Since the main cause of IL is the volatility of the token pair, it would be right to assume that liquidity providing with a less volatile pair would result in little to no impermanent loss. There are many stablecoin pools on different platforms. For example, USDT/USDC LP on Babyswap, or DAI/BUSD on Alpaca Finance.

· Liquidity providing with low volatility pairs. If both tokens are moving in one direction most of the time, it is safer to invest in them than in other, more volatile pairs. Some tokens’ values are pegged to others so by investing in them you’ll minimize IL risk. mSOL/SOL pair is one example. But don’t forget that occasionally the pair can depeg from each other. For instance, a lot of capital was invested in the TOMB/FTM pool when the token TOMB was pegged to FTM. But FTM price is almost 10 times of that of TOMB now.

· Single-sided staking pools. This type of staking allows investors to earn yield for providing liquidity only for one asset. For example, you can add LUSD on Liquity to improve its solvency. Or you can add USDT to the liquidity pool on Stargate. To find one-sided staking pools you can go to Beefy Finance (app.beefy.finance), and select “Single Assets”.

· Flexible liquidity pool ratio. A typical 50:50 ratio that is employed by most AMMs increases the likelihood and magnitude of IL. Flexible weights offered by Balancer, such as 80/20 pools result in less IL than ordinary 50/50 AMM pools.

· Selecting pools with high trading fees. When users add funds to liquidity pools, those funds are used for trading purposes. Trading using these pools pay fees part of which is distributed by automated market makers to liquidity providers. Trading fees can decrease the burden of impermanent loss; they can even be sufficient to totally cover the effect of IL.

· Waiting. As we mentioned earlier, if liquidity provider doesn’t withdraw funds from the pool, IL is not realized. So one solution to hedge IL is just waiting for exchange rate between two tokens to return to the level at which you entered the pool. Let’s say, you entered ETH/DAI pool when 1 ETH was worth 1,000 DAI. Then, ETH goes to 1,500 DAI within a short period. If you think this jump was not sound and the price will revert to the previous level, you can choose to wait to avoid IL.

· Another, more complex solution to impermanent loss is power perpetuals. Power perpetuals track the price of the underlying asset raised to a power. For example, SOL2 simply is the power perpetual whose underlying is SOL price squared.

The main reason to trade power perpetuals instead of ordinary perpetuals is that they exhibit option-like characteristics. The value of the normal assets can be written as (1+r) where r is the return in percent. However, return on the power perpetual squared will be (1+r)2 = r2 + 2r +1. You can think of the power-2 perpetual as a 2X levered normal perpetual because of this 2r.

In constant product AMMs impermanent loss can be written as

IL = 2 * ( — 1 — r/2)

where r is the price change expressed as %.

It is possible to expand as Taylor series as follows:

= 1 + r/2 — r2/8 + r3/16–5r4/128 + …

Now our formula for IL becomes

IL = 2 * ((1 + r/2 — r2/8 + r3/16–5r4/128 + …) — 1 — r/2)

Since 1 and r/2 terms cancel out, we get

IL = 2 * (– r2/8 + r3/16–5r4/128 + …) = — r2/4 + r3/8–5r4/64 + …

Cubic and higher-order terms can be ignored for hedging purposes because they will be vanishingly small. Therefore, our goal should be to hedge the quadratic term. Let’s express both impermanent loss and power perpetual as functions of the initial price:

IL = 2 * p * (-r2/8). This is what we want to hedge

Power2 perpetual = p * (1 + r)2

After simplifying the expressions, it turns out that to hedge our LP position against IL we should buy power perpetuals. We should also sell ½ regular perps because buying a power perpetual has a delta which should be hedged away. So, to achieve a sufficiently good hedge against IL through power perpetuals we can

Buy power perpetuals, where p is the initial price

and sell ½ regular perps.

· Lending protocols. If you add liquidity to the ETH/USDC pool and ETH price goes up significantly, you will lose money due to IL. But if you borrow ETH on a lending protocol against your USDC deposit, you’ll decrease ETH price risk. Since you are holding ETH now, even if ETH price increases and causes an impermanent loss in your LP position, you’ll have hedged your investment.

· Bancor, one of the first decentralized staking protocols, has designed a novel way to hedge against impermanent loss. What it does is to transfer the risk from liquidity providers to the exchange protocol itself. Some pools have high trading fees and low IL, while others have low trading fees and high IL. If there are enough fees, the protocol will cover the negative effect of IL; (is it necessary to add?) if there aren’t, more BNT will be minted.

Their insurance policy will increase at 1% each day after a liquidity provider adds funds to the pool. Insurance will be fully mature after 100 days which means if you withdraw your funds after 100 or more than 100 days, you’ll be fully insured against any loss due to IL. If you withdraw, say, after 70 days, only 70% of the compensation will be distributed to you. If you decide to withdraw funds within the first 30 days, you’ll not be compensated for any impermanent loss incurred. It’s as if you provided liquidity at an ordinary AMM without any insurance policy.

Because of high market volatility, Bancor has suspended its impermanent loss insurance policy in June 2022.

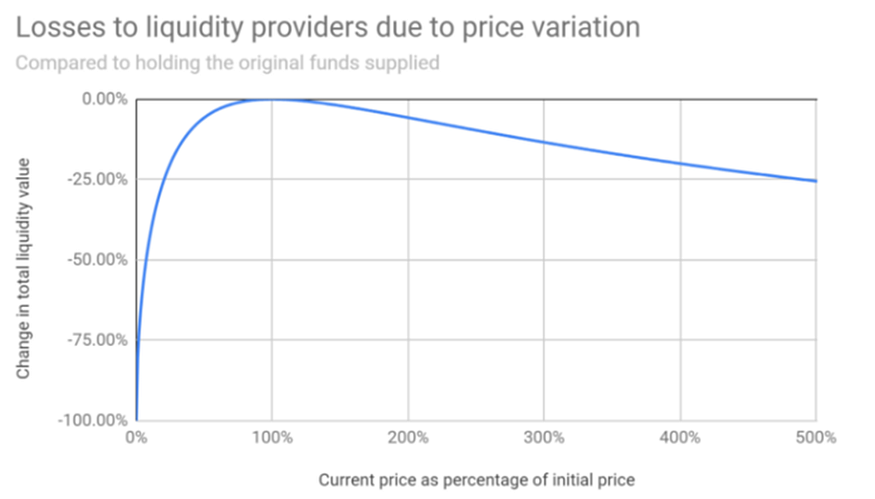

· Out-of-money (OTM) options. If a token goes up by 100% or goes down by 50%, loss incurred by IL will be 5.7%. To hedge against such strong moves, one can consider buying OTM put and call options.

Say, you add liquidity to ETH/DAI when ETH price was $1,500. If ETH jumps to $3,000 or plunges to $750, your impermanent loss will be 5.7%. To hedge this risk, you can buy a call option with the strike price of $3,000 and a put option with the strike price of $750. The problem with this strategy is that crypto options, especially such deep OTM options may not be too liquid.