The adage is being proven that no technology can ever gain mass adoption until it proves its usefulness to the masses. The complicated regulations and market restrictions in developed countries are making penetration of new technologies near impossible without proof of their effectiveness and application elsewhere. This is precisely where the markets of underdeveloped countries are starting to demonstrate their potential for application of blockchain technologies.

Around the world in prospects

The world is a massive market of opportunities for new technologies and the Middle East and Africa (MEA) region remains an untapped treasure-trove in terms of blockchain application.

Analytical company IDC forecasted blockchain spending to be $2.7 billion in 2019 — an increase of 80% over 2018. While the current growth rate is quite impressive, it still represents a small portion of total internet technology spending. As a comparison, IDC projected investment in new technologies such as the Internet of Things, artificial intelligence, and virtual reality to have reached $961 billion in 2019.

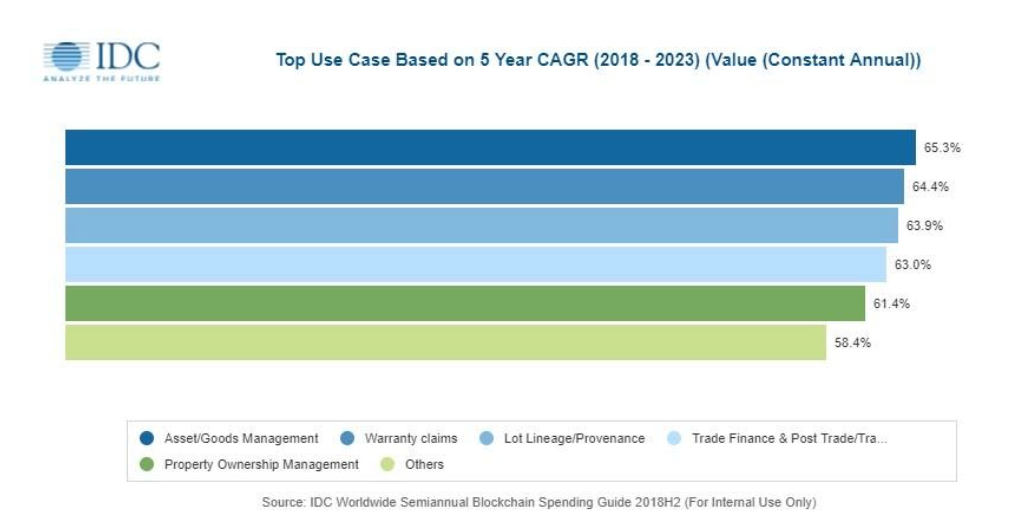

Image source: IDC

The IDC report stated that MEA nations are set to increase their spending on blockchain to $105 million by 2023, up from $21 in 2019, which represents 50% annual growth. The main drivers of adoption are state authorities seeking to bolster their public administration and security capabilities.

Notably, the European Union (EU) is trailing not far behind as the European Commission is exhibiting great interest in blockchain technologies. The European academic community is also acting as a driver for technology development and political acceptance. Investments in blockchain in the EU amounted to $661 million in 2019.

Meanwhile, the United States is still the best environment for blockchain development, given its strong academic basis and technological advancement. The regulatory framework remains the main obstacle, but it is not hindering the US’ leading positions in investments in blockchain. The amounts invested by the country’s government in blockchain last year amounted to $1.1 billion, outstripping any competitor by a long shot.

The Asian region is just as progressive in terms of blockchain adoption with China investing as much as $304 million in the sector in 2019. President Xi Jingping made it clear that blockchain is critical to China’s economic prospects. As such, China dominates spending on blockchain in the region with 70% of all contributions on development. Neighboring Singapore is also claiming that blockchain is fundamental to the nation’s economic development.

The wider Asia-Pacific region together taken is set to spend up to $2.4 billion on blockchain development by 2022, according to IDC. The report forecasts a spike in blockchain spending, predicting around $523.8 million in 2019 — an increase of 83.9% from $284.8 million in 2018. Between 2018 and 2022, the IDC expects a five-year compound annual growth rate of 77.5%. Overall contributions from the regions amounted to 18.4% of all blockchain spending in 2019, third after the EU with its 23.7%, and the 37.7% of the US.

Delving deeper

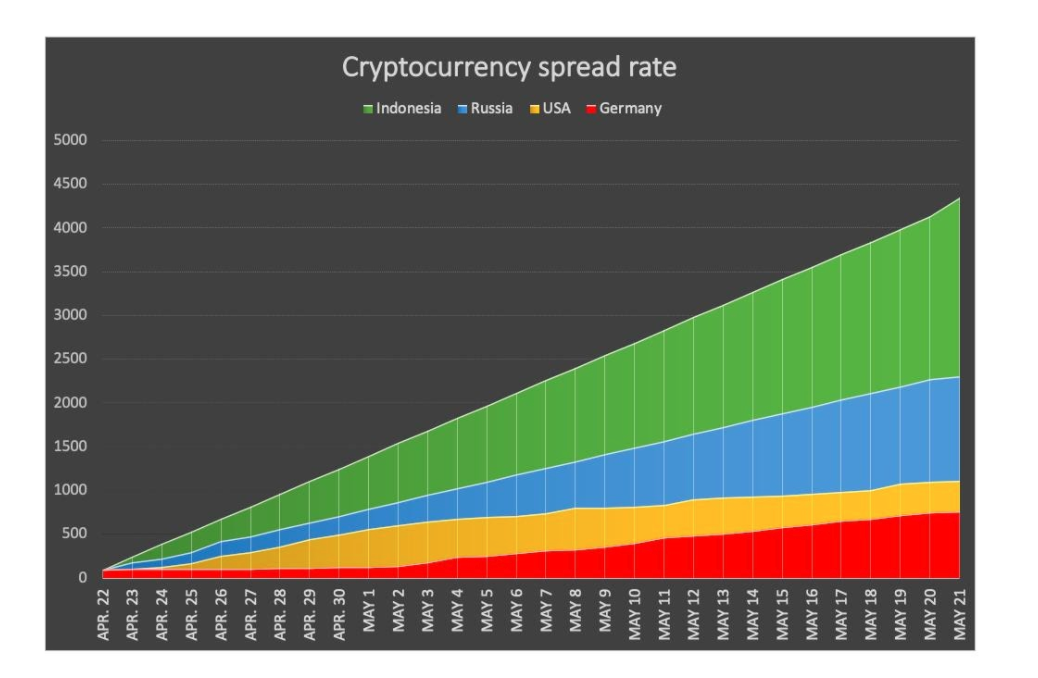

Blockchain project ONFO recently conducted a social mining experiment in a number of countries to determine the popularity and permeation of blockchain and crypto assets amount local populations. Four countries were chosen for the research – the US, Germany, Indonesia, and Russia. The first two states were designated as developed nations and the latter two as developing ones.

The experiment foresaw the distribution of free crypto assets to 100 individuals in each country with an average of ten coins per person. The participants would be able to receive more coins for attracting additional users. The results of the experiment demonstrated that participants from developing nations exhibited four times more activity than those in developed nations. The ONFO report summarized that 100 people in the US attracted 1,120 additional users, 100 German users attracted 763 new participants, while Russian participants managed to gain the interest of 2,034 people. Indonesia outstripped the other three nations twofold by attracting 4,350.

ONFO founder J.R. Forsyth is confident that the spread in developing nations was considerably greater due to the fact that small amounts of money bear greater value there. Forsyth also noted that Indonesia demonstrated “massive growth” potential for crypto assets.

“Indonesia possesses the unique conditions that make it well-poised for Bitcoin adoption. As the world’s fourth most populous country, it’s home to a largely cash-based community, and huge swaths of the population — up to 80% — remain unbanked,” as Forsyth stresses.

Image source: ONFO

The US and Indonesia are similar in their population sizes, which allowed ONFO to draw several conclusions. 14% of the US population uses cryptocurrencies, compared to 11% in Indonesia. However, the contrast resides in the fact that US citizens were accustomed to crypto assets in 2008-2010, while Indonesia started on the path merely 1-2 years ago.

Indonesia rising

A report released by GlobalWebIndex states that 11% of Indonesians own crypto assets. Taking into account that Indonesia is the fourth most populous country in the world, the statistics demonstrate that each 9th Indonesian is a participant of the crypto industry.

Such a massive level of adoption places the country in 6th position in the global ranking on mass adoption after the Philippines, Brazil, South Africa, Thailand, and Nigeria. One of the main reasons is the devaluation of the national Indonesian Rupee, which was hard-hit by the economic crisis of 1998 and has since surged in 2020 by 18%.

In addition, internet penetration in the country is as high as 64%, making it fertile ground for cryptocurrency use and greater penetration with adequate educational activities.

Africa leading

While the Asia-Pacific region is boasting considerable progress in blockchain adoption and cryptocurrency usage, the African continent bears just as much potential for penetration.

Africa is a highly-promising market due to the particularities of the local economies, where inflation rates are high and fiscal policies can wax and wane overnight. Local conflicts and political turmoil also contribute to financial instability, making cryptocurrencies favorable savings instruments.

The local remittances market is also a contributing factor with its $48 billion annual volume, transaction commissions of 9% and mobile transfer payment fees reaching 11%. The advantages of using cryptocurrencies with their low commissions and decentralization become obvious.

Change is coming

The challenges to mass blockchain and crypto adoption remain low electrification in rural areas, poor education levels, and a lack of clear standing on digital assets from as much as 60% of local governments.

The global financial crisis and the ongoing pandemic are making it clear that developing countries will be the drivers of growth in the technological sector. The 70% share of services in the economies of developed countries will make their recoveries longer and more demanding. It is possible that adoption can and should start from unsaturated markets that have the necessary economic conditions for highlighting and accentuating the main properties of blockchain and crypto technologies.