Many experts are convinced that the world is on the brink of a global crisis, the approaching of which accelerates the trade war between the U.S. and China, gradually covering other countries.

The role of central banks in opposing export-oriented economies is growing noticeably. For example, the stimulating monetary policy of the regulators, which often implies quantitative easing, not only revives business activity, but also has a positive impact on national exports due to devaluation.

However, the fascination of central banks with soft monetary policies can exacerbate trade wars and reinforce the global trend towards protectionist barriers that affect international trade. This, in turn, will lead to a fall in stock indices, a decline in the return on investment in traditional assets, as well as a decline in the development of the entire global economy.

In this article, ForkLog Magazine will talk about the declining effectiveness of traditional monetary policy instruments and the risks of quantitative easing, the impact of central banks on the course of trade wars, as well as why Bitcoin can become a hedging instrument in the coming economic crisis.

What is the role of central banks in financial crises?

Central banks - regulators that have a significant impact on the monetary sphere, national currency rate, inflation rate, business activity, and the state of the economy as a whole.

Using classical monetary policy instruments, central banks (CB) periodically change the key rate, mandatory reserve requirements, perform currency interventions and open market operations.

All of these instruments have worked relatively well in the past decades, when even developed countries were characterized by relatively high inflation rates by current standards. Over time, however, the economic growth of developed countries began to slow down, as did inflation, and traditional monetary recipes began to lose their effectiveness. For example, the decline in the Fed's key interest rate, even to record low levels, has increasingly slowed business activity in the United States

To solve this problem in the late 80s of the last century, a completely unconventional monetary policy tool called Quantitative easing (QE) was used for the first time. Its essence is that the central bank, which buys or secures various assets from banks and other private companies, serves as a source of liquidity for the financial system and stimulates the national economy.

In the United States, this policy was actively pursued after the global financial crisis, from September 2012 to October 2014. According to the IMF experts, in the short term QE contributed to the reduction of systemic risks, increased confidence in financial institutions and mitigated the consequences of the recession.

However, in the medium to long term, this approach entails serious risks. For example, QE can lead to significant inflation and, in the context of the global economy, to financial bubbles. In addition, the increase in the monetary aggregates leads to devaluation of the local currency against other monetary units, which stimulates national exports.

It is worth emphasizing that in modern conditions such an approach involves significant risks, given the trade war between China and the United States. Soon after Trump's announcement that by devaluing the renminbi to increase the competitiveness of exports, China "rapes" the United States, the giant countries began to confront each other.

Over time, trade confrontation has only increased, offsetting the advantages of the free market, spreading to other countries and bringing the global crisis closer. Recently, the U.S. president announced the introduction of a 5% duty on all goods imported from Mexico. According to Donald Trump, such a measure will help stop the flow of illegal migrants.

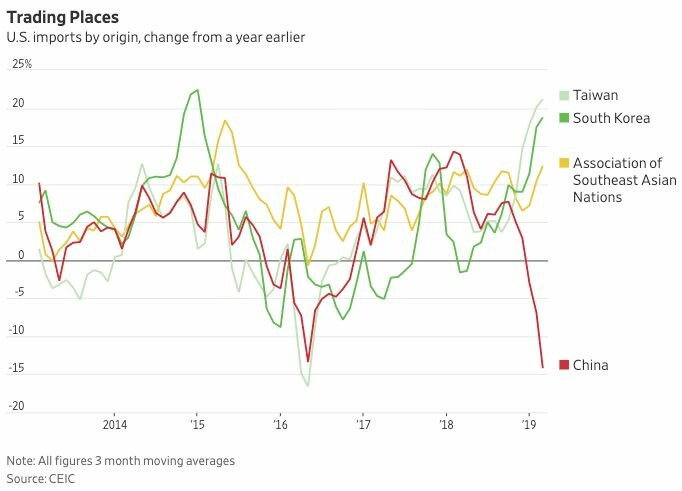

The chart below illustrates the consequences of the growing confrontation between the U.S. and China:

U.S. import dynamics from Asian countries.

As can be seen, imports from China have fallen significantly. This cannot but affect world trade as a whole, given the volume of industrial production in the Celestial Empire, trade turnover with the U.S. and the degree of China's participation in international cooperation and specialization.

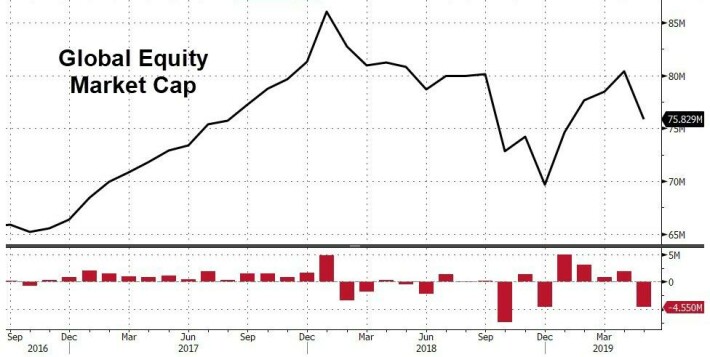

However, the global stock markets have already reacted to the confrontation between the two giants - in May their capitalization fell by $5 trillion:

Source: ZeroHedge

Anatomy of the financial crisis

Let's look in detail at what a financial crisis is, how it manifests itself, why it is hitting developing countries the hardest and how central banks are trying to mitigate its effects.

The financial crisis (FC) systematically covers financial markets and institutions, money circulation and credit, international, state, municipal and corporate finance.

At the macro level, the crisis has a medium- and long-term negative impact on economic activity in the country and on the dynamics of the welfare of the population. In the financial sector it is manifested in:

a sharp rise in interest rates;

a growing number of troubled credit institutions;

accumulation of bad debts;

Reduced lending;

the wave of bankruptcies;

Decrease in investment activity;

Securities depreciation;

Reduced liquidity of financial markets;

bank panic, etc.

In international finance, the FC finds expression in:

uncontrolled depreciation of the national currency;

large-scale capital flight from the country;

external debt growth;

transfer of systemic risk to the international market and financial systems of individual countries.

In the context of money circulation, the FC is often expressed in the form of acceleration of inflation, and in the field of public finance - in a sharp decline in international reserves and state stabilization funds, a decrease in tax revenues and budget deficit, cuts in public spending and growth of domestic public debt.

Developing economies are the most vulnerable to the global financial crisis. The latter are weaker in comparison with developed countries, lack a significant reserve of financial strength, are externally dependent and permeated by various deformations.

As a rule, social and political risks are high in developing countries. At the same time, financial systems are unbalanced and characteristic of them:

lack of resources;

high volatility and risks;

Significant inflation and interest rates;

limited resources of banks and institutional investors;

dependence of the economy on external markets and foreign investments.

As a result, underdeveloped countries are most vulnerable to market shocks, so-called "financial infections" (the transfer of economic shocks from one country to another and the concerted fall of markets). These economies are also characterized by significant capital flight.

Financial crises are caused:

- internal causes: national economic cycles that are secondary to the global ones, over-concentration of certain risks, political instability;

- external influences: global economic cycles, financial infections leading to devaluation and currency crisis, speculative attacks, etc.).

Systemic risks, arising in one market link (private crises), then extend to other links in the market, in some cases causing the collapse of the entire financial and credit system of the country. Private crises include:

- debt securities;

- stock market;

- bank and currency.

Any of these crises may arise against the background of relatively favorable conditions in other segments of the financial and monetary spheres and serve as a kind of trigger mechanism, transforming negative local phenomena into a large-scale financial crisis.

In addition, during the crisis, many economies are inclined to lock themselves in. For example, if the crisis comes from outside, protectionist measures and counteraction to capital flight are intensified. Globalization seems to be shrinking.

Many countries are implementing Keynesian measures to stimulate domestic demand and increase investment. This is done through fiscal methods (public investment, tax incentives, various measures to address unemployment), as well as through the central bank (quantitative easing, refinancing of credit institutions, reduction of interest rates and required reserves).

In export-oriented economies, the national currency is devalued to stimulate import and export substitution and improve the trade balance.

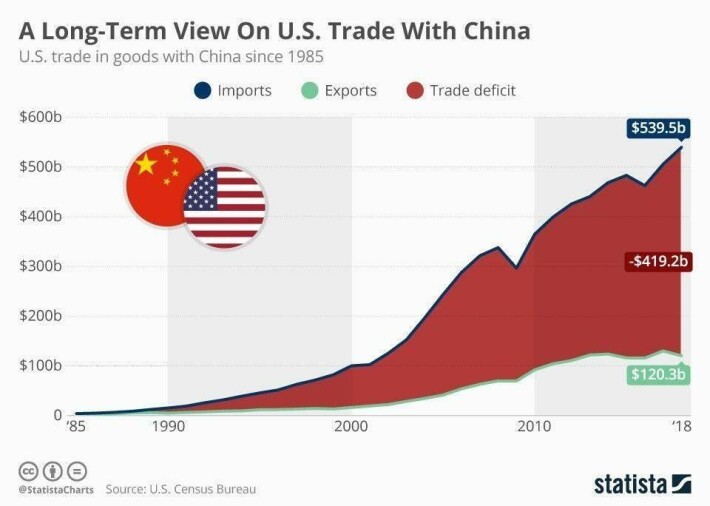

The image below shows the extent to which imports from China to the US exceed exports:

The US trade deficit has been growing rapidly since 1990.

According to Bloomberg, many investors and prominent experts have no doubt that the Fed will reduce interest rates in the coming months to make exports more competitive and imports more expensive to reduce the trade deficit.

Thus, in the context of trade wars and financial crisis, monetary regulators have a significant role to play. Let us now consider why central banks are in many ways responsible for the huge imbalances in the global economy, which make the crises deeper and their consequences more comprehensive and truly disastrous.

Global economy and monetary alchemy

Michael Pento's article "A Brief History of Financial Entropy" says that with the collapse of the Bretton Woods system, the U.S. dollar has been finally freed from the gold peg. As a result, the global monetary system has got rid of any restrictions on the growth of the monetary base.

After 1971, new opportunities opened up for the rapid growth of financial markets and complex derivatives. In addition to floating courses, this process was facilitated by scientific and technological progress and, in particular, by the growth of computing power, which significantly increased the scale of financial transactions and the speed of the latter.

In the first half of 1987, stock markets grew rapidly. However, after the U.S. federal government announced a larger than expected trade deficit, there was a decline in the dollar and a rapid collapse of the markets, nicknamed black Monday. Due to globalization and the systemic nature of risks, the stock markets of Asia, as well as Australia, Canada and the United Kingdom, soon found themselves in a free fall.

The newly appointed head of the Federal Reserve Board, Alan Greenspan, has taken innovative measures, thanks to which the central bank served as a source of liquidity for the stock market and the financial system as a whole.

"For the first time since its inception in 1913, the Federal Reserve Board has not just come to the aid of a single bank, not just tried to create incentives for economic growth. Greenspan made it clear that the central bank is now directly supporting the stock market," said Michael Pento.

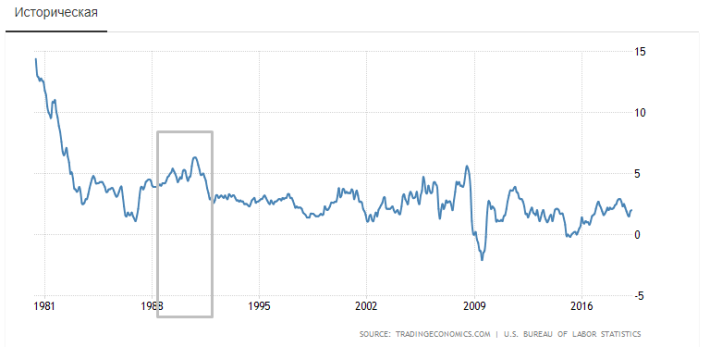

The graph below shows inflation trends in the United States since 1980:

As can be seen, in the late eighties, the inflation rate in the U.S. increased significantly, which is likely to be closely related to the quantitative easing undertaken by the Federal Reserve. Data: tradingeconomics

In the late 1990s, the Asian financial crisis broke out. It was triggered by the extremely rapid growth of Asian tiger economies, which contributed to massive investment inflows, public and corporate debt growth, and real estate market boom. In addition, the overheating of the economies was significantly exacerbated by the rampant growth in lending, which led to the accumulation of bad debts.

One of the main reasons for the crisis in Asia was the mild policy of central banks and passion for foreign borrowing, resulting in a fall in national currencies, stock indices, rising inflation and corporate debt, and a wave of high-profile bankruptcies.

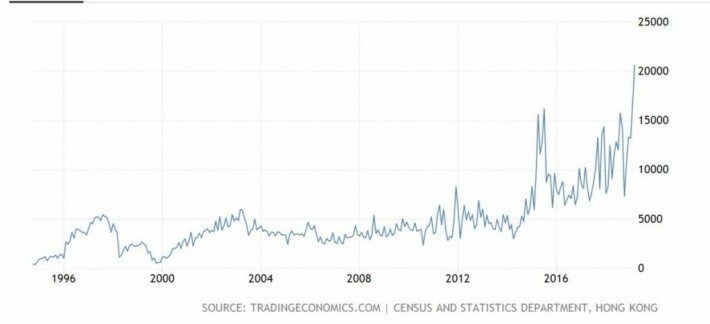

The number of bankruptcies in Hong Kong has been growing rapidly over the past few years. Moreover, the sharp jump in bankruptcy rates occurred in the spring of 2019, which may indicate an acceleration of the crisis processes. Data: tradingeconomics.

Financial infection from Asia spread rapidly to many countries around the world. In particular, the fall in commodity prices and capital outflows contributed to the Russian crisis in 1998. The latest echo of the "Asian contagion" is the Argentine default of 2001.

The NASDAQ bubble, which was authorized by the U.S. authorities to print money by the year 2000, after the collapse of which the shares of technological companies lost 78% of their value by the fall of 2002. At the peak of this bubble, the total market capitalization of shares as a percentage of the country's GDP was already far from 66% and 148% of GDP.

After the dotcom bubble collapsed, the Federal Reserve reduced interest rates to 1%. Such a low level was maintained for one year, from June 2003 to June 2004. This led to overheating of the real estate market and later to the global financial crisis of 2007-2008.

The Fed's response to the worst crisis since the Great Depression was to reduce interest rates from 5.25 per cent in 2007 to almost 0 per cent by the end of 2008. The regulator also made a quantitative easing by purchasing assets from banks worth $3.7 trillion and creating another bubble.

According to Michael Pento, much of the responsibility for the emergence of bubbles in the markets and extremely deep crises lies with the central banks, which are fond of stimulating monetary policy:

"As a result of the increase in interest rates, access to cheap credit, which keeps unsustainable businesses afloat, is blocked. Recessions are useful because they save the economy from unproductive investments. However, due to the systemic and destructive practice of artificially restraining interest rates, central banks have created conditions for large-scale and inefficient placement of capital. This has led to unprecedented debts and huge asset bubbles.

The expert believes that the unprecedented growth of household debts and excessively inflated stock market make the economy extremely vulnerable.

Even a small decline in GDP can quickly provoke a real avalanche of defaults and economic chaos," says Pento. - The power that once belonged to the free markets was completely usurped by governments and central banks. The truth is that Wall Street cares very little about corporate profits and the economy, but instead focuses entirely on every word coming from the mouth of the central bank.

The shape of the coming financial crisis

Daniel Lacalle, the economist of the Tressis hedge fund, is convinced that one of the main factors behind the development of the financial crisis is the so-called demand-side policy, which encourages investors to believe that there is no risk due to the "pillow" of the government and the central bank. Because of this, most assets are perceived as risk-free or protected. Also, crowds of market participants in the run-up to the crisis tend to think that "this time it will be different".

Among the main direct triggers of the crisis the expert considers sovereign debt to be the main one, against which abnormally low yields of government bonds are restrained by the policy of central banks. The latter, the economist is sure, is like a placebo effect. However, in the end, this effect disappears and losses accumulate.

"When markets fall, they fall at the same time," said Lacalle.

The situation is further exacerbated by the fact that the widespread impact of central bank activities makes it much more difficult to analyse potential losses.

"There is a widespread belief that monetary policy has been highly effective, growth has been sustained and shared, and debt growth is only a side effect, but not a global problem. This has led to harmful arrogance and increased imbalances. The crisis of 2007 broke out because in 2005 and 2006, even the most cautious investors were drawn to risky financial instruments," added the economist.

Lacalle is convinced that a crisis is inevitable and its onset is only a matter of time. Nevertheless, he believes that the new crisis will not be similar to the previous one.

"Financial infection will spread much more slowly as the Lehman falls have been learned. Now there are stronger mechanisms to avoid a major domino effect in the banking system.

On the other hand, as in 2007-2008, the problem of the next crisis will be seen by many only on the surface, in the symptoms (as in the case of the bankruptcy of Lehman Brothers). However, the real cause of the crisis will be an aggressive monetary policy that "encourages risk taking and punishes prudence".

A difficult problem, Lacalle says, is that the next crisis will catch up with the central banks defenseless: "without the tools to disguise structural liquidity problems. In addition, the situation is greatly complicated by the record volume of global debt.

Analysts at Morgan Stanley are convinced that in response to the almost inevitable recession caused by the trade confrontation between the two giant countries, the central banks will react by all means to the easing of monetary policy.

Currency restrictions are already tightening in various countries. For example, last year Chinese banks were instructed to give out only up to $5,000 in cash. In other cases, the clients of financial institutions must provide the reasons why they needed this amount in foreign currency. The trend towards currency restrictions is likely to intensify in a new crisis.

Bitcoin as a hedging instrument in a global crisis

The challenges of crises at the macro- and global level are extremely complex and require an integrated approach to their analysis. This analysis is extremely complicated by the uncertainty and entropy caused by the above-mentioned "monetary alchemy" of central banks.

Some supporters of the Austrian school of economics question the monopoly power of monetary regulators, whose actions are often ineffective, non-transparent and unpredictable. According to the "Austrians", central banks are dependent on governments, and their mistakes have disastrous consequences for consumers in the form of inflation (reflected in rising commodity prices) and sharp increases in interest rates (leading to higher borrowing costs).

At the same time, central bank countermeasures aimed at reducing inflation suppress economic activity and lead to unemployment. On the other hand, in order to revive business activity, the regulators are setting unnaturally low interest rates, which are causing bubbles in the real estate market and financial sector.

Proponents of the Austrian school also note a significant difference between sustainable economic growth, funded by private savings, and unsustainable problem growth, which is stimulated by loans from the central bank.

Among the "Austrians" there are a lot of supporters of the gold standard, who believe that with this model the boom and bust phase does not last long, because the market, free from abuse of regulation, quickly finds a balance. For example, in the XIX century, when the central banks kept reserves in gold and did not know about QE, the "great depressions" fit into the framework of one, rarely two years.

With the fall of this system, central regulators have significantly increased their ability to offer cheap money, keep abnormally low interest rates and issue unsecured funds to banks. It became possible to prolong the boom phase with a corresponding deepening of the decline phase.

However, despite the vast opportunities offered by modern technology, it is unlikely that monetary regulators will give way to monopoly power without a fight. Despite all the drawbacks of modern central banks, for the vast majority of countries these institutions are the dominant structures for economic management.

At the same time, many experts are confident that the answer to the imperfection of monetary policy will be Bitcoin and other cryptocurrencies, the popularity of which will increase with the aggravation of global crisis phenomena.

"I'm not saying that the fiat money will disappear. However, given the way in which central banks carry out monetary policy and the size of government debt, all this will have a positive impact on the price of Bitcoin," says Think Markets UK analyst Naim Aslam.

Michael Moreau, the head of Genesis Global Trading, is confident that Bitcoin is becoming an increasingly attractive alternative asset in an environment of extremely low interest rates. According to Moreau's observations, the BTC price and the Fed rate have a negative correlation. This may indicate that many investors are already considering the first cryptocurrency as an alternative asset to hedge risks.

"In 2018, when the Fed raised interest rates, the return on investment in Bitcoin was low," the analyst shared his observations.

Travis Kling, investment manager of Ikigai Asset Management, is confident that the vast majority of central banks are significantly politicized.

"As policies and monetary instruments intertwine, investors use digital currencies as a means of protecting themselves from irresponsible fiscal and monetary policies," said Kling.

Thus, in the context of declining interest rates and quantitative easing, as well as the development of crisis phenomena in the global economy, demand for bitcoin and other cryptocurrencies can be expected to increase.

Advantages and disadvantages of Bitcoin compared to fiat money

Unlike fiat money, Bitcoin is not controlled by a central regulator and is therefore free of "monetary alchemy". In particular, the parameters of the first cryptocurrency are strictly defined in the program code, which makes its emission predictable.

To make cryptocurrency payments, there is no need for intermediaries, and transactions are inexpensive, fast, reliable and accessible to everyone. The recipient of funds can be a user from anywhere in the world. There are also cryptocurrencies that provide a high degree of privacy.

Recently, Binance, the largest stock exchange in terms of trading volumes, has moved Bitcoin by $1.26 billion, with a commission of only $124.6. According to representatives of Weiss Ratings, such an insignificant amount of commission for the transfer of more than an impressive amount raises the question of the need for financial intermediaries in the form of banks.

Nevertheless, the mass acceptance of Bitcoin and other cryptocurrencies is still a long way off. For example, in some countries, including India, Algeria, Bangladesh, Bolivia, Pakistan, Macedonia and Vietnam, virtual currencies are banned. Authorities in these countries view new assets as volatile and highly speculative surrogates that undermine money circulation, threaten financial stability, and are used to launder money and support terrorism.

Nevertheless, the authorities of many countries see the cryptocurrencies as something innovative and self-sufficient, weakly controllable, but with noteworthy features. It's not easy for some central banks to actively explore blockchain's possibilities and even think about releasing their own digital currency.

Are the digital currencies of the central banks viable?

Recently, the National Bank of Ukraine (NBU) reported that within the framework of the pilot project for the introduction of the "Electronic Hryvnia" (e-Hryvnia) platform, it continues to study the possibilities of launching its own digital currency and even issued a number of coins.

"Our research gave us not only practical experience, but also gave rise to new questions for the National Bank. What will be the impact of this instrument on the payment market ecosystem? Will the demand for e-hryvnia be sufficient for users, sellers and market participants? What technology should be used? What should be the level of anonymity of e-commerce transactions? Today, not only we, but also other central banks of the world do not have the exact answers to these questions," said Deputy Head of the NBU Sergei Kholod.

While the NBU is only studying the advantages and disadvantages of central bank digital currency (CBDC), some experts call on regulators to step up efforts to issue innovative monetary units.

For example, the Avenir Suisse analytical center suggests that the National Bank of Switzerland should develop an economic model based on blockchain. The next step is the creation of the so-called "franc-token", which is controlled by the central bank of staplecoin. Experts are confident that the new coin will facilitate trade in tokenized securities, facilitate trade finance and create new business models.

The head of the Bank of Lithuania Vitas Vasiliauskas is also optimistic, convinced that CBDC can act as a means of exchange, payment and preservation of value. Also, he is sure that the state cryptocurrencies can increase the efficiency of payments and settlements in securities and reduce various risks in the financial market.

However, regulators in some countries are skeptical. Thus, the president of the German Federal Bank Jens Weidmann believes that cryptocurrencies issued by central banks can destabilize financial systems and worsen the performance of credit institutions, especially during the crisis. He also believes that demand for CBDC may have a negative impact on the efficiency of the central regulator and contribute to a fundamental shift in the business model of banks.

"There's no real breakthrough in technology yet," Weidman said.

A similar view is held by the Deputy Head of the Bank of Japan, Masayoshi Amamiya, who doubts that the CBDC can improve the efficiency of monetary policy.

The Bank of Russia report "Does the digital currencies of central banks have a future?" states that government cryptocurrencies can reduce transaction costs, as well as be effective in low interest rates and low inflation. In addition, CBDC accounts can also be credited with interest, making such coins an attractive means of preserving value.

On the other hand, the document specifically notes that "to date, there are no successful, fully functional and accessible CBDC to the general public, including those based on distributed registry technology.

Overall, some 70 per cent of central banks around the world are studying the feasibility of creating digital public currencies, but only a handful of them have started to implement projects.

"Compared to 2017, the number of banks starting experimental work with digital currencies increased by 15%. However, most of the projects are analytical and do not indicate that banks have specific plans to issue such assets. Only five banks managed to create usable pilot projects," the Bank for International Settlements said in its report.

It is difficult to say what advantages central banks' cryptocurrencies have for the financial system, or whether they will take root at all. On the other hand, in some countries, Bitcoin, which has been in existence for over 10 years, is not only popular, but is perceived by many as a means of preserving value, competing with the national currency.

For example, in Venezuela, which suffers from hyperinflation, the demand for the first cryptocurrency is huge. The people of this oil-rich country use seemingly highly volatile cryptocurrencies to make daily payments and buy the essentials.

The economic situation in Argentina is not so acute, but also difficult, where Bitcoin has reached its absolute maximum, paired with the local peso currency, due to galloping inflation.

"If an Argentinean had bought Bitcoin at the highest point of the "greatest bubble in history" in 2017, he would now have more money than if he had deposited it in a bank account," said cryptocurrency trader Josu San Martin.

Thus, while central banks are exploring blockchain, Bitcoin and other cryptocurrencies are successfully leveling out the state's failures.

***

Due to the soft policies of central banks, the resulting devaluation of national currencies and the global economic crisis, many developing countries will demand Bitcoin and crypto-assets as a means of preserving value.

In the face of declining returns on traditional assets, investors from developed countries and institutional investors will view the cryptocurrency more as a tool for portfolio diversification.

The crisis and the depreciation of fiat money will undoubtedly contribute to the growth of demand for Bitcoin and other assets and their mass acceptance. The role of cryptocurrencies in the global financial and political systems is already becoming increasingly important.

Central banks are likely to continue to study distributed registry technology, assessing the advantages and disadvantages of publicly produced digital currencies. However, regulators and other experts now assess the advantages and disadvantages of CBDC in different ways and pay attention to all kinds of risks, casting doubt on the feasibility of issuing innovative monetary units.

Central banks, despite all their shortcomings, are unlikely to cede their monopoly power to cryptocurrencies. However, the latter will increasingly compete with fiat money, which will lead to serious changes in the monetary policy of regulators and banking systems of various countries, as well as further tightening of the regulation of the cryptocurrency industry.

Subscribe to Bitcointime.eu News