Markets do not usually panic because of what central banks do. They panic because of what central banks suggest they might do next.

That is exactly what happened after Kevin Warsh’s first Federal Reserve meeting as chair. On paper, the decision looked simple: the Fed kept interest rates unchanged. No surprise cut. No surprise hike. Just a pause.

But investors were not really listening for the rate decision itself. They were listening for reassurance. They wanted to hear that rate cuts were still possible, that inflation was under control, and that the new Fed chair would offer a clear roadmap for the rest of the year.

Instead, they got something colder, shorter and more uncertain.

Warsh delivered a message that sounded less like a promise of easier money and more like a warning: inflation is still a problem, the Fed is not ready to cut, and markets should stop expecting the central bank to guide them by the hand.

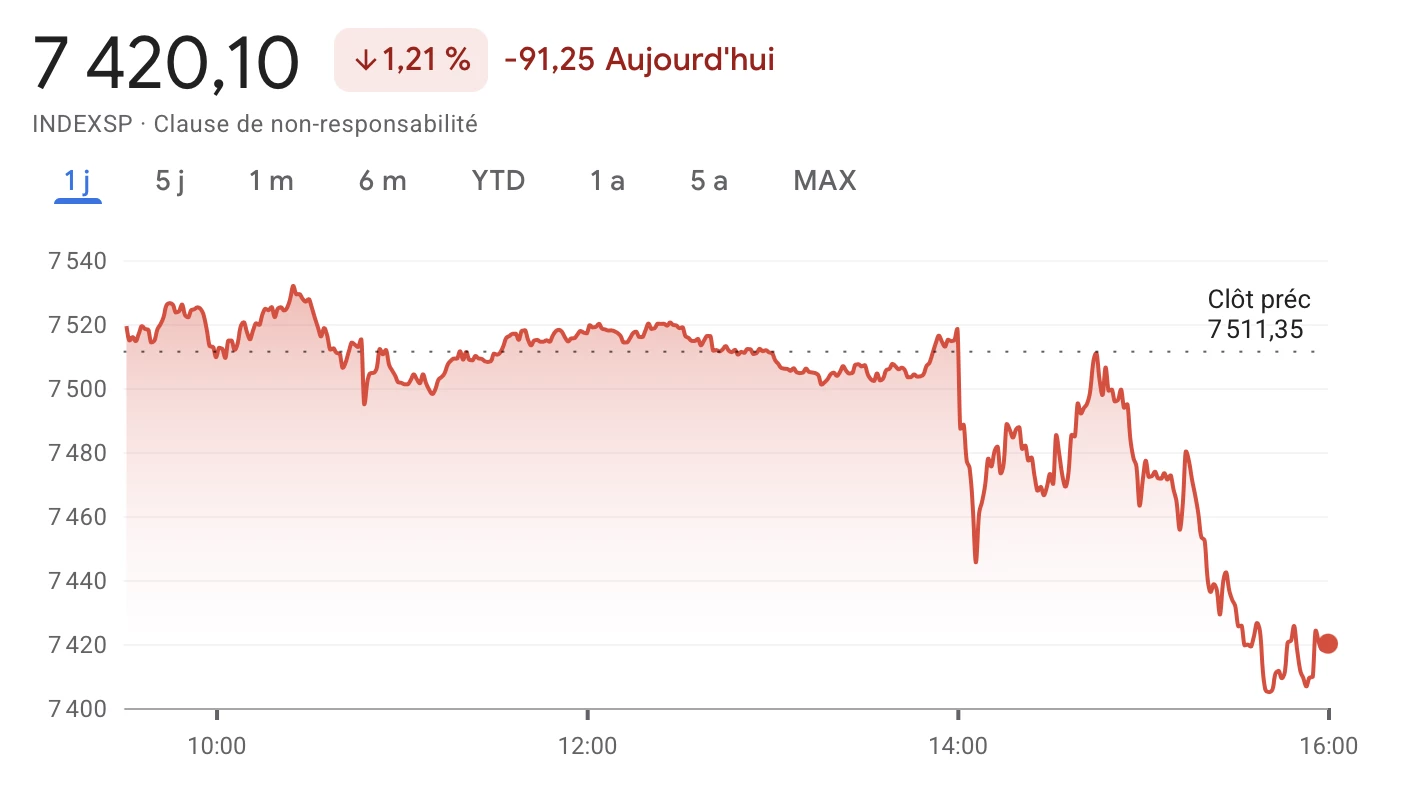

That was enough to push stocks, Bitcoin, gold and other risk-sensitive assets lower.

1. The Market Expected a Softer Fed — It Got a More Cautious One

The first reason markets fell is simple: investors had positioned themselves for a friendlier Federal Reserve.

Kevin Warsh arrived at the head of the Fed with a political story already attached to him. Donald Trump had wanted a central bank chair more open to lowering rates than Jerome Powell. Many investors assumed that Warsh’s arrival could mark the beginning of a more accommodative policy cycle.

That assumption turned out to be too optimistic.

Instead of opening the door to rate cuts, Warsh kept rates unchanged and emphasized the need to bring inflation back toward the Fed’s 2% target. The message was not aggressive in the theatrical sense. He did not shock markets with an immediate hike. But he also did not give investors what they wanted.

And sometimes, disappointment is enough.

The market had been hoping for a pivot. What it received was a pause with a hawkish undertone.

That matters because modern markets are extremely sensitive to interest rate expectations. When investors believe rates will fall, they are usually more willing to buy risk assets. Lower rates make cash less attractive, reduce borrowing costs, support corporate valuations and increase the appeal of long-duration assets such as technology stocks and crypto.

But when the Fed signals that rates may stay higher for longer — or even rise again — the calculation changes.

Suddenly, investors become more defensive. Treasury yields move higher. Equity valuations come under pressure. Crypto loses part of its liquidity narrative. Gold can also weaken if real yields rise.

That is why the reaction was not limited to one asset class. The sell-off reflected a broader repricing of risk.

Warsh did not crash the market by changing rates.

He moved the market by changing expectations.

2. The Fed Removed the Comfort Blanket of Forward Guidance

The second reason investors reacted badly was Warsh’s communication style.

For years, markets have grown used to a Federal Reserve that explains itself in detail. Since the 2008 financial crisis, central banks have relied heavily on forward guidance: carefully crafted language designed to tell investors what policymakers are likely to do next.

That system gave markets something to anchor to.

Even when the Fed was uncertain, investors could analyze every word, compare statement changes, study projections and build scenarios around the central bank’s tone. The result was not perfect clarity, but at least a sense of direction.

Warsh appears to want a different Fed.

His first statement was shorter and more direct. It offered fewer clues about future policy. He also signaled that the Fed may rethink how it communicates, how it uses data and how it presents forecasts to the public.

For economists, this may sound like an institutional reform. For traders, it sounds like less visibility.

And markets hate less visibility.

Investors do not need certainty, because certainty rarely exists. But they do need a framework. If the Fed removes too much guidance, markets must price a wider range of outcomes. That means more volatility.

The reaction after Warsh’s speech was therefore not only about interest rates. It was also about the rules of communication.

A less talkative Fed may give itself more flexibility. But that flexibility comes at a cost: investors no longer know exactly how to interpret the central bank’s next