TVL down 39%. More than 40 protocols down, $840 million stolen in five months. But at the same time, Apollo Global, BlackRock and Morpho just furthered their relationship. The tale is not as simple as either side would like to make it.

It's been a rough start to 2026 for DeFi. TVL fell from ~$115 billion in January to ~$70 billion in June, a decrease of 39%. It was the worst month in the history of the sector, as more than 30 different exploits were used to make a total of just under $635 million for attackers. Over 40 protocols were completely closed. The news was grim.

But that's not the only thing Apollo Global Management, which manages assets of almost $940 billion, has done: it's strengthened its ties with one of DeFi's key lending protocols, Morpho. BlackRock's tokenized U.S. treasury fund has been added to Uniswap. Curiously, institutional DeFi activity is on the rise while retail activity is diminishing.

To get the both/and part, you must understand what DeFi is, how it works, and what has changed over the six years it has existed.

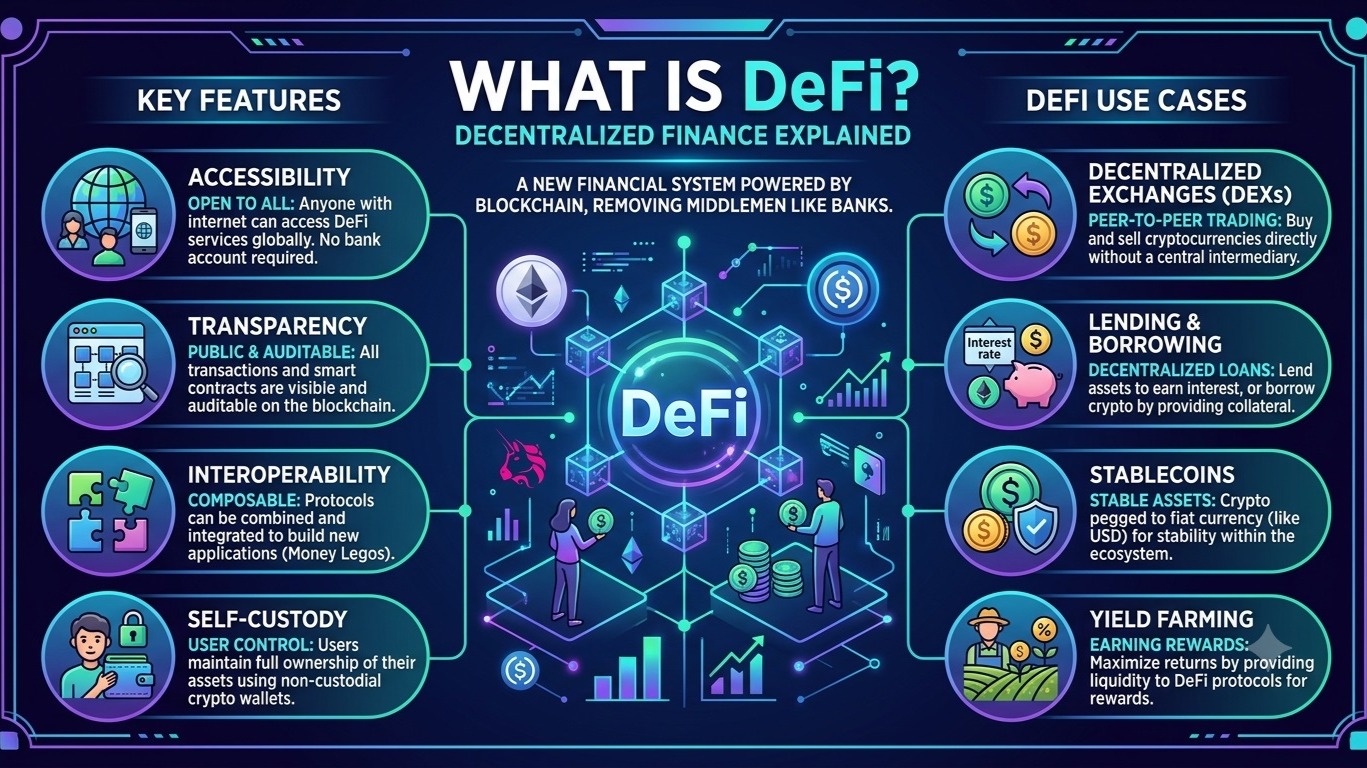

What DeFi is: No jargon.

Decentralized Finance is an umbrella term for financial services provided by blockchain smart contracts instead of traditional financial institutions like banks or brokers. Lending, borrowing, trading, earning interest — all automated by code, open to anyone with a crypto wallet and an internet connection, and without a company in the middle taking a cut, running 24 hours a day.

The principle behind DeFi is straightforward: most of the financial intermediaries, such as banks, stock brokers, clearinghouses, etc., are required because someone has to manage the books, enforce the rules and trust. Smart contracts take care of all that automatically. Altogether, the bank is the code. When you put ETH into the lending protocol, it stores them, applies the interest to them, and withdraws them when you withdraw. There is no discretion by anyone. No business hours. No credit check. No geography restrictions.

That's the promise. As 2026 has shown, the execution is not quite that simple.

The work of the main products.Description of the action of the main products.

DEs (decentralized exchanges) include Uniswap, Curve, PancakeSwap, and others that enable you to swap one token for another without the need to use a centralized exchange like Binance or Coinbase. They have liquidity pools (LP) rather than an order book where buyers and sellers can match, which are large repositories of paired tokens which can be accessed by anyone who wants to contribute a portion of the trading fees to the LP. You are not trading with another user, you are trading with the Uniswap pool when you sell ETH for USDC. The price automatically updates based on the ratio of the assets in the pool.

Lending protocols such as Aave, Morpho, Compound operate as decentralized banking systems. You put in crypto as collateral and can borrow against it. The borrowers pay the depositors interest. The distinguishing factor from conventional lending – they are always over-collateralized. You have to spend more than you borrow, because there's no credit check, no legal protection in case of any default. If the value falls below the ratio of the protocol, the liquidation of your collateral is done automatically. No phone call or no negotiation — the smart contract sells it!

Liquid staking is a particular challenge in proof-of-stake blockchains, and as of May 2026, Lido boasts a TVL of $20.89 billion. The ETH that is being staked to secure the network is locked up. You get a yield and cannot use the assets. Lido creates a derivative token (stETH) for you that is representative of your staked ETH and may be utilized in the remainder of the DeFi sector as you continue to earn staking rewards on your ETH. It's yield stacking, which is staking plus anything else you can do with the derivative token.

It is this concept that Restaking — EigenLayer — extends. It allows you to stake your existing ETH to protect multiple networks and protocols and receive multiple streams of yields from a single investment. The concept is on capital efficiency. The downside is you're now putting the same piece of collateral for multiple systems, and if one of them fails, it can impact all of them. This interconnection can spread shocks as seen in the KelpDAO exploit in April 2026.

What happened in April 2026?What took place in April of 2026?

April was the worst month for DeFi yet, and the way it played out is instructive because it shows how the basic dangers of DeFi are more clearly manifested than any theory.

The first breach was the Drift Protocol hack that cost $295 million. In a social engineering attack, the Lazarus Group was operating inside the project for six months, obtaining a level of inside access that a smart contract audit can't catch. Next came KelpDAO: a $292 million exploit of their cross-chain bridge. The bridge had one verifier, a single point of failure, to validate cross-chain messages. It was used by attackers to steal assets and borrow real money with it later on the Aave protocol.

The spread of the contagion rapidly accelerated. The fact that rsETH — the token being used to liquid-stake KelpDAO — had been used as a broad collateral across DeFi made the exploit effectively have been unstaking. Aave lost $8.45 billion in deposits in 48 hours. The overall TVL on the DeFi market dropped by $13.21 billion over 2 days. Aave's bad debt grew to an estimated $123-230 million. Withdrawals took place on protocols that have no direct exposure to KelpDAO, as it has been observed that a shock wreaks havoc on DeFi's interconnections across the entire network.

In total, the two April attacks – Drift and KelpDAO – together took more than 50% of crypto DeFi losses in 2026. Lazarus Group is thought to have been responsible for both. The same North Korean hacking group that stole $1.5 billion from Bybit in February 2025. Now they represent about 76% of the total losses resulting from cryptocurrency hacks worldwide. Security is a major part of DeFi's issue is a geopolitical issue.

The procedures that did survive—and why.

The 2026 correction did something good: it weeded out the few protocols that were alive on the back of speculating and inflows on token sales and got rid of those that still were. There are some factors which all the survivors have in common.

Aave kept operating and was even solvent with $8.45 billion in deposits lost in the KelpDAO crisis. It saw its TVL drop from $26.4 billion to $14.3 billion, a sad but not catastrophic decrease. At a time when the crisis was calmed, the protocol's deep liquidity in conjunction with conservative risk parameters and a decade-long track record made it credible and brought in deposits again. As of April 2026, Aave V3 is deployed on 15+ EVM chains with TVL of $19.4 billion, which is the greatest among all DeFi lending protocols.

Through the downturn, Lido has been the top pure DeFi protocol by TVL at $20.89 billion. Its fee mechanism is such that it earns consistent income from staking rewards, rather than emissions that are lost as speculations die down. This is the business model you can build that will keep you afloat during the bear market.

It was Apollo Global's desire to target specific markets and earn superior returns that made Morpho a partner they wanted to work with, despite the fact that it has $5.8 billion in TVL, compared to Aave's $11 billion. The most obvious sign is that up to 9% of Morpho's governance tokens are now in the hands of Apollo with no doubt that the institutional capital views DeFi lending as a credible credit market rather than a sideshow.

The protocols that failed had the inverse profile, with tokens that had lost 70–90% of their value in dollars, no revenue from fees, strong reliance on incentive emissions to bring liquidity, and no institutional relationships to shore them up during retail capital runaways.

Should it be done again in 2026?

This is subject to the entity of comparison and the type of risk you can bear.

For yield: Lido's liquid staking currently provides an annual yield of approximately 3-4% on ETH. Aave's lending markets also have variable rates when it comes to stablecoins that are usually in the range of 4-8% on USDC, depending on utilization. Around 4-5% tokenized Treasury products such as the BUIDL by BlackRock are backed by US government bonds. The interest rate differential is narrowing between DeFi and traditional finance, as interest rates climbed. DeFi was providing 20–100% interest rates in 2020 — seemingly free money. The realistic DeFi yields in 2026 will still be in line with money market funds but not by a wide margin.

Smart contract risk is very real and uninsured for the risk you are taking on. The total amount of losses on DeFi, recorded by DefiLlama, is not a fictional one.The $7.6 billion losses in DeFi, as recorded by DefiLlama, is not a theoretical amount. About 28% of these are lent protocols. Bridge incidents made up the biggest single incidents. An audit will minimize risk, but will not remove risk. If one oracle fails, bridges are compromised, or vaults are. . . . . months of yield can be lost in minutes. The issue isn't if DeFi returns are appealing on their own. It's whether they're appealing on the back of the odds of potential pitfalls.

DeFi is still the only financial infrastructure that is truly open, 24/7 and without identity verification or borders for anyone in the world. That's a legitimate and substantial benefit to a large percentage of the world's population. A user in Argentina who adds $50 to the wallet on Aave can access this earning 5% deposit, which a US money market fund can't. That's an example use case that is indifferent to yield spread on Treasuries.

It is the move that tells you what.It is the move which tells you what.

The signal that is most useful at the moment in DeFi is not TVL. It's been that big-cap names like Apollo, BlackRock and Fidelity are investing in it, and retail investors are taking their money. Schools are unlike most other places, and they don't move quickly toward what they don't believe will be there in ten years. The dollar amount of $940 billion is an asset manager buying governance tokens in a DeFi lending protocol, and at the same time the market is in great fear, you can tell a lot about where the smart money is going.

What remains after 2026 will be different DeFi than what exists in 2020. A reduced speculation of yield farming. Increased institutional lending and settlement. More efficient protocols, less in number. DeFi is not dying, it's consolidating, as evidenced by the 40+ shutdowns that are happening this year. Of course, the question is which protocols are on the right side of this consolidation and that answer is becoming clearer each and every month.

The best advice for anyone new to DeFi in 2026: keep it simple and go with the big cap tokens. Lending is done on Aave, staking on Lido, and swapping on Uniswap. These are battle-tested protocols which have been operating on the live network for years and have already billions of dollars worth of proven liquidity. Consider anything newer, smaller, or more recent to be high-risk allocation—the type that can be damaged what-you-give-to-receive allocation. And store your seed phrase offline. For most individual users, the largest risk of DeFi is not a bridge exploit, it's a phishing link and wallet emptied in seconds.